Capital Carbon Expands rCB Capacity To Tackle Supply Chain Issues

- By Gaurav Nandi

- January 14, 2025

The Tamil Nadu-based company’s greenfield expansion will propel its rCB capacity from 5,000-20,000 metric tonnes. Director Ravi Rathi explained that there has been a change in attitude towards rCB within tyre companies, leading to heightened demand.

Tamil Nadu-based Capital Carbon is expanding its recovered carbon black (rCB) capacity by 15,000 metric tonnes with a new greenfield project at Gummidipoondi. The plant is slated to become operational by January 2025 and boost the capacity from 5,000 metric tonnes to 20,000 metric tonnes, annually.

Speaking to Tyre Trends, Director Ravi Rathi explained, “The decision to pursue a greenfield expansion in the rCB sector stemmed from the rapid development of this innovative product over the past four to five years. Given our background in the pyrolysis business, expanding into rCB felt like a natural progression. rCB is still a relatively new product and both manufacturers and users are in the process of learning about its applications. When we first began exploring this market, around four years ago, it was challenging. Many tyre manufacturers would dismiss our proposals even before we could present our case as they were hesitant to incorporate recycled materials into their mainstream formulations.”

“However, in recent years, attitudes have shifted significantly due to increasing emphasis on sustainability and circular economy principles. The industry is now more open to integrating green products. We started with a modest capacity of 5,000 metric tonnes per annum, which allowed us to gain insights into customer needs. Gradually, we scaled our operations from small quantities to commercial sales. The key driver for our recent expansion is customer demand. We have obtained product approval, and customers are eager to purchase rCB,” he added.

“However, in recent years, attitudes have shifted significantly due to increasing emphasis on sustainability and circular economy principles. The industry is now more open to integrating green products. We started with a modest capacity of 5,000 metric tonnes per annum, which allowed us to gain insights into customer needs. Gradually, we scaled our operations from small quantities to commercial sales. The key driver for our recent expansion is customer demand. We have obtained product approval, and customers are eager to purchase rCB,” he added.

He also noted that companies wanted assurance that the demands could be met consistently, which was also a factor behind the expansion. Furthermore, having multiple units also allows the company to manage any potential supply chain issues, effectively. “If a minor problem arises in one unit, we can still supply material from another, minimising disruptions for our customers,” said Rathi.

The entire CAPEX for the greenfield plant is set at INR 20 crore.

Pyrolysis to rCB

Capital Carbon commenced operations in 2012 with a modest pyrolysis capacity of 10 tonnes per day. Over the years, it has consistently expanded its capacity, increasing to 150 metric tonnes per day. The company has also bolstered its backend operations, enhancing sourcing capabilities and adding substantial shredding and crumbing capacity.

Additionally, Capital Carbon has focused on value-added products including pyrolysis oil distillation and rCB. As of now, it operates a shredding capacity of 120,000 metric tonnes per annum for captive consumption. This capacity is supplemented by sourcing contaminated tyre bales, which typically have 20-30 percent rubber contamination. This material is cleaned to yield 98 percent pure steel, with the remaining rubber used for pyrolysis, creating a separate business vertical.

Currently, the company processes approximately 50,000 to 52,000 metric tonnes of tyres per annum through its pyrolysis operations. In terms of value addition, Capital Carbon produces between 20,000 to 24,000 tonnes of pyrolysis oil, annually.

When asked about the motivation behind establishing a pyrolysis plant, Rathi noted, “My father worked at Birla Carbon and retired in 2019. Although we lacked prior business experience, we were inspired by the industrial upbringing and the promising potential of the pyrolysis sector. Following the completion of my chartered accountancy studies, I decided to pursue this opportunity.”

He acknowledged that pyrolysis often has a negative reputation in India, where it is sometimes viewed as a ‘dirty business’. To combat this perception, Capital Carbon prioritises quality management and environmental responsibility in its operations. IT employs fuel-based heating methods in its pyrolysis process as electric heating is generally not feasible due to the high volumes involved in tyre pyrolysis. The initial heating requires some fuel, which can include biomass or pyrolysis oil, but the system becomes self-sufficient once it reaches a certain temperature.

The primary outputs from the pyrolysis process include fuel oil, carbon char (used as raw material for rCB or as an alternative energy source for cement plants), steel wires and pyrolysis gases, which are utilised for heating purposes.

He highlighted that the pyrolysis oil produced is of high quality with low sulfur and carbon content, making it cleaner than many conventional heating fuels used in India.

Quality control

The company’s sourcing strategy primarily focuses on domestic suppliers. It procures rejected tyres and dealer returns from various companies, which constitute a substantial portion of the feedstock. This local sourcing approach ensures that it maintains a steady supply of raw materials

Following sourcing, the production of recovered carbon black involves several critical steps. Initially, tyres are shredded to extract carbon black, steel and other components. The distinction in product application necessitates tailored processing methods.

For instance, producing carbon char for energy requires less stringent technical specifications compared to producing carbon black intended for high-performance applications, such as tyre manufacturing or footwear.

“The quality of the final product begins with meticulous sorting of tyres to determine suitability for pyrolysis. This initial step is vital for ensuring consistent output quality. Following sorting, the tyres are shredded into steel-free rubber chips of 15-20 millimetres. During pyrolysis, we focus on maintaining specific quality parameters for the pyrochar produced. This includes stringent controls to limit ash content, which must remain below 20-22 percent to ensure product consistency. The handling of impurities such as wires and stones in the pyrochar is essential. Post-processing, the pyrochar is milled to fine particle sizes (10-15 microns), enhancing its surface area for better compatibility with rubber compounds,” explained Rathi.

Once the recovered carbon black is processed, palletisation becomes the next step. This method streamlines handling and ensures that the product meets industry standards. While the equipment resembles that used for traditional carbon black, adaptations are necessary to accommodate the unique characteristics of recovered carbon black.

“To facilitate customer adoption, we offer tailored packaging solutions including 25kg paper bags, EVA / LDPE bags and FIBC bags, allowing clients to integrate our products seamlessly into their existing production processes,” he added.

As the industry evolves, the need for standardised quality benchmarks for recovered carbon black has become increasingly clear. Major corporations have driven this change, leading ASTM to establish a dedicated committee (D36) focused on developing specific standards for recovered carbon black. Unlike conventional carbon black, which adheres to existing standards, recovered carbon black requires new metrics to account for its varied origins and compositions.

The committee is currently validating a series of standards including moisture content, pallet hardness and particle size analysis, specifically for rCB. This ongoing development is slated to enhance product credibility and facilitate broader market acceptance.

Commenting on the same lines, Rathi mentioned, “We maintain a dedicated quality lab to refine our production processes continually. Our focus on evolving our offerings has resulted in the introduction of two new grades of recovered carbon black, aimed at meeting diverse market needs. Our commitment to leveraging advanced machinery and improved grinding techniques reflects our proactive approach to quality enhancement and capacity expansion.”

Optimistic market outlook

The demand for recovered carbon black in India is poised for significant growth, driven by a strong shift toward sustainability. Customers are increasingly seeking high-quality suppliers, indicating a burgeoning market for rCB.

“Globally, rCB production currently accounts for less than one percent of total carbon black production, underscoring a substantial opportunity for expansion. As customer awareness and demand for sustainable products increase, we anticipate a corresponding rise in rCB consumption,” informed Rathi.

He added, “Many major corporations have committed to achieving carbon neutrality by 2050, necessitating immediate action to integrate green and circular products into their supply chains. As these companies strive to meet their net-zero targets, they are turning to recovered materials such as rCB to fulfil sustainability mandates. Our role is crucial in assisting these customers to achieve their goals through the production of eco-friendly and circular products derived from end-of-life tyres.”

Speaking on market opportunities, he said, “India remains our largest market, but we are also making significant inroads into Sri Lanka. The European market is particularly promising, though it presents challenges related to certifications and distribution. We are currently working on obtaining the necessary certifications, including ISCC Plus, to unlock this market potential.”

“Our immediate focus is on completing our current expansion project, after which we will enhance our pyrolysis capacity to align with the growing demand from our customers. As the volumes of recovered carbon black usage increase, we aim to be ready with sufficient supply,” he added.

He expects to penetrate the European market by the first half of FY26, following the completion of the current plant expansion.

Challenges in scaling production

“One of the primary challenges in scaling rCB production is the scarcity of raw materials. The supply of suitable feedstock is diverse and scattered, making it difficult to source consistently. In the past, customers struggled to understand the differences between recovered carbon black and virgin carbon black grades, often asking if we could produce specific grades like L550 or L660. However, as knowledge in the market has matured, customers are increasingly recognising that rCB is a distinct material requiring tailored processing approaches,” informed Rathi.

Zeon And Yokohama Rubber Advance Sustainable Rubber Project With New Facility Completion

- By TT News

- August 04, 2026

Zeon Corporation has finalised the construction of a new bench-scale facility at its Tokuyama Plant in Shunan City, Yamaguchi Prefecture, dedicated to advancing the efficient production of butadiene from sustainable ethanol sources. The project, which broke ground in July 2025, represents a strategic move to establish a naphtha-independent raw material supply chain, thereby bolstering both corporate sustainability and the broader transition towards a carbon-neutral society. The facility is slated to commence full-scale operations in January 2027, with the ultimate goal of achieving commercial viability by 2034.

A commemorative ceremony took place at the plant site on 31 July 2026, drawing a total of 46 attendees. The gathering included official representatives from Japan’s Ministry of Economy, Trade and Industry (METI), the New Energy and Industrial Technology Development Organization (NEDO) and local governmental bodies from Yamaguchi Prefecture and Shunan City. Also present were delegates from the Yokohama Rubber Company, the construction contractor and various affiliated firms, alongside Zeon’s leadership, including Akira Honma, the Corporate Officer and Tokuyama Plant Manager.

This initiative forms one half of a dual-themed research and development programme undertaken in partnership with Yokohama Rubber, under the auspices of NEDO’s Green Innovation Fund. The collaborative effort is focused on the social implementation of technologies for synthesising both butadiene and isoprene from renewable biological materials by the 2030s. As part of this process, Zeon is set to produce a prototype polybutadiene rubber using the output from the new bench-scale facility, while Yokohama Rubber will subsequently manufacture test tyres from this material and conduct performance evaluations on test tracks.

Both companies have outlined a clear roadmap, intending to finalise the core technology for societal deployment by 2030 through the operation of a larger pilot plant, with full-scale commercialisation targeted for 2034. The bench-scale facility is a critical precursor in this phased approach, providing essential data for the scale-up process.

The broader project encompasses two selected NEDO themes, both subsidised through the Green Innovation Fund. The first involves the highly efficient synthesis of butadiene from ethanol, with technical cooperation from the National Institute of Advanced Industrial Science and Technology. The second focuses on biotechnological pathways to directly produce butadiene and isoprene from plant-based materials, involving partnerships with the Institute of Science Tokyo and RIKEN. Both tracks aim to supplement synthetic rubber feedstocks and support closed-loop recycling, aligning with Japan’s 2050 net-zero emissions goal by fostering long-term industrial innovation.

- Association of Natural Rubber Producing Countries

- ANRPC

- Monthly NR Statistical Report

- Natural Rubber

ANRPC Publishes Monthly NR Statistical Report For June 2026

- By TT News

- July 31, 2026

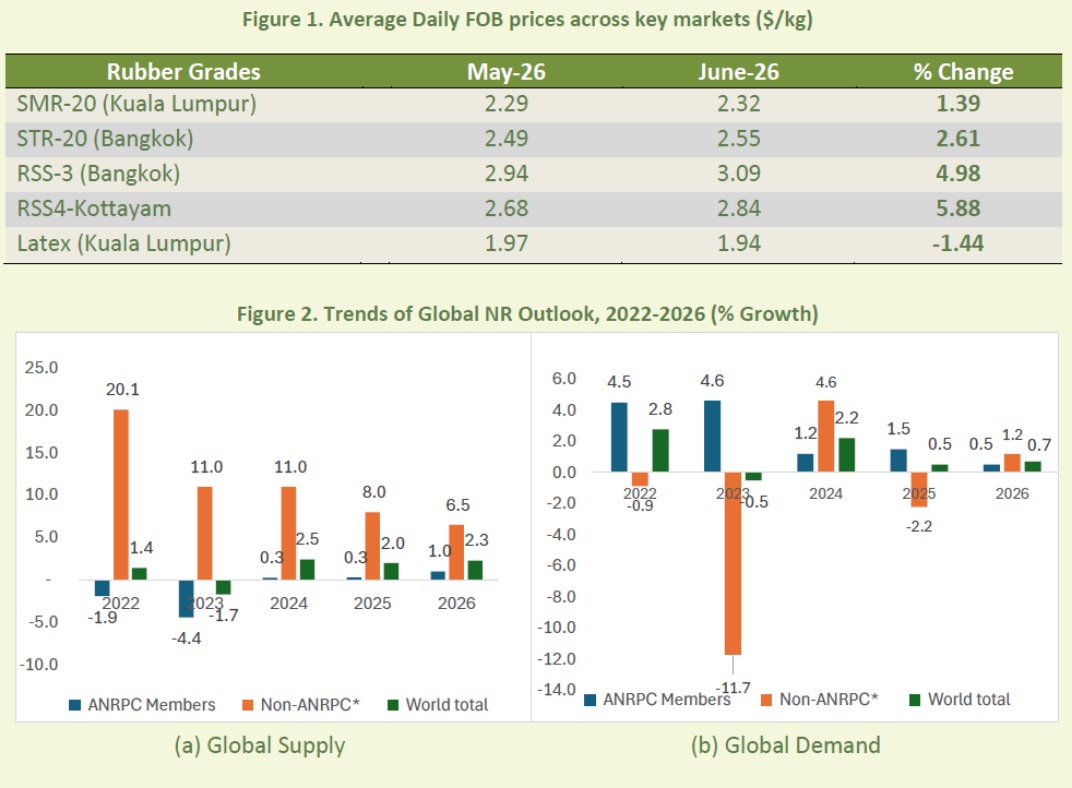

The Association of Natural Rubber Producing Countries (ANRPC) has released its Monthly Natural Rubber Statistical Report for June 2026, a month defined by price resilience amid conflicting market forces. The provisional reopening of the Strait of Hormuz triggered a sharp 20.29 percent drop in Brent crude oil prices to USD 85.40 per barrel. However, this bearish signal was counterbalanced by persistent supply constraints from El Niño-related weather disruptions across major producing regions.

Physical rubber prices posted broad-based gains across most grades. SMR-20 rose 1.39 percent to USD 2.32 per kilogramme, while STR-20 gained 2.61 percent to USD 2.55 per kilogramme. RSS-3 and RSS-4 advanced 4.98 percent and 5.88 percent to USD 3.09 and USD 2.84 per kilogramme, respectively, though latex eased 1.44 percent to USD 1.94 per kilogramme. On the trade front, China's imports surged 7.14 percent month-on-month, while India and Viet Nam declined. Export growth was recorded for Cambodia, Viet Nam and Indonesia, though Thai shipments contracted.

Global production for 2026 is projected at 15.310 million tonnes, up 2.3 percent from 2025, driven by gains in Thailand, China, India and Malaysia. However, June output fell 3.7 percent year-on-year to 1.207 million tonnes due to seasonal wintering and El Niño-related weather disruptions. Malaysia, Indonesia and Cambodia have introduced new incentive and governance measures to strengthen their sectors. Global consumption is forecast to grow 0.7 percent to 15.411 million tonnes in 2026, with June consumption rising 3.3 percent to 1.300 million tonnes, led by China and India amid steady tyre and EV-related demand.

Currency markets saw the Malaysian ringgit trade between RM3.96 and RM4.08 against the US dollar, while the Thai baht ranged from 32.56 to 33.24. In futures trading, the SHFE September 2026 contract averaged 17,580.68 CNY per tonne, down 0.45 percent month-on-month, while the SGX September contract averaged USD 2.24 per kilogramme, up 1.75 percent, with both reflecting tightening supply and firm downstream demand.

Pyrum Secures Long-Term Supply And Offtake Agreements With Pirelli

- By TT News

- July 31, 2026

Pyrum Innovations AG has finalised long-term supply and offtake agreements with Pirelli, reinforcing the tyre manufacturer’s European Tyre-to-Tyre initiative. The deal secures Pirelli’s purchase of Pyrum’s ThermoTireBlack (TTB) for use in its European production facilities, while Pirelli will provide Pyrum with end-of-life tyres from designated German sources.

These contracts simultaneously bolster Pyrum’s feedstock security and guarantee an industrial outlet for its recycled materials, covering both raw material procurement and product commercialisation. Through its proprietary thermolysis process, Pyrum transforms scrap tyres into ThermoTireBlack, which can substitute fossil-based carbon black, and ThermoTireOil (TTO), destined for chemical industry use. The partnership offers further validation of Pyrum’s technology within a certified European value chain involving tyre, chemical and synthetic-rubber leaders.

Pyrum also supports the broader Tyre-to-Tyre project, initiated by Pirelli with BASF and Synthos, which reintroduces secondary materials from used tyres and production waste into new tyre manufacturing via an ISCC PLUS-certified, traceable system.

Pascal Klein, CEO, Pyrum Innovations AG, said, “Signing these long-term agreements with Pirelli is an important commercial and strategic milestone for Pyrum. The coöperation secures both the supply of end-of-life tyres and an industrial outlet for our TTB. It confirms that our technology and products meet the requirements of one of the world’s leading tyre manufacturers and can contribute to the establishment of scalable circular value chains in Europe.”

MICHELIN ResiCare And IMCD Europe Forge Strategic Distribution Partnership For 5-HMF

- By TT News

- July 30, 2026

MICHELIN ResiCare, a specialist in renewable and high-performance chemical solutions, has entered into a distribution partnership with IMCD Europe, a major international distributor of speciality chemicals. The agreement centres on the European supply of 5-hydroxymethylfurfural (5-HMF), a bio-sourced compound produced at the company's Isère-based industrial facility in Péage-de-Roussillon.

Under the new arrangement, IMCD Europe will handle distribution across the continent while MICHELIN ResiCare maintains direct engagement with its key strategic accounts. The collaboration aims to significantly widen the molecule's availability to European manufacturers through an optimised logistics framework and localised technical support, thereby addressing rapidly growing demand within the materials and formulation chemical sectors.

The French production site, scheduled to begin operations in early 2027, will have an initial annual capacity of 3,000 metric tonnes. This domestic manufacturing capability represents a critical step in securing European access to a molecule deemed strategically important for the region's chemical industry, reducing reliance on external supply sources.

IMCD will contribute its technical expertise, market knowledge and pan-European distribution network to facilitate the integration of 5-HMF into new applications. The company's established footprint in polymers, advanced materials and speciality formulations positions it to provide developmental support to manufacturers exploring alternatives to fossil-derived intermediates. MICHELIN ResiCare has already spent two years assisting major industry players with application evaluations, and the partnership is expected to expand these efforts across a broader customer base.

Derived from fructose through non-toxic green chemistry and already REACH-registered, 5-HMF serves as a versatile building block for low-environmental-impact resins and can replace conventional petroleum-based ingredients across diverse industries including agriculture, cosmetics, construction, transport, aeronautics and electronics. The collaboration reinforces MICHELIN ResiCare's commitment to renewable resources and sustainable material development while aligning with IMCD's dedication to advancing innovation in greener chemistry solutions.

Laurent Lemonnier, CEO, MICHELIN ResiCare, said, “This partnership with IMCD represents a major step forward in our desire to popularise the use of 5-HMF and to support the transition to a more responsible chemistry. With its technical expertise, its capacity to support customers and its European location, IMCD is the perfect partner to speed up the distribution of this molecule of the future.”

Comments (0)

ADD COMMENT