THE ANSWER: COLLECTIVE FARMING

- By Dr. Siju T

- October 19, 2020

The state of Kerala in southern India still accounts for over 70% of the tappable area and 75% of the national rubber production in India. Given the agro-climatic advantage, quality of human resources cultivating rubber and productivity of rubber, Kerala is expected to retain its prime position in Natural Rubber production in the near future. Though the area under rubber cultivation is increasing in the non- traditional regions, which has got cost advantages over the traditional region, it has inherent climatic disadvantages. A cost-benefit analysis by RRII revealed higher BCR (Benefit-Cost Ratio) for Kerala than in the non-traditional regions due to its higher productivity which offsets the higher cost in the state to some extent. So, maintaining the production sector in Kerala in good health is key to ensuring sufficient domestic production of rubber in the coming decades as envisaged in the National Rubber Policy (NRP) of India.

The NRP envisages sourcing 70% of India’s requirements of natural rubber through domestic production. This also gains importance as India has once again started thinking in the direction of self-sufficiency through its Atma Nirbhar Bharat initiative and the current domestic production of Natural Rubber accounts for just over 50% of the national requirement.

But the days of the smallholding sector of Kerala, which has scripted the success of rubber production in India from the 1980s onwards, seems to be over and running out of steam. The sector is in deep crisis as it is confronted with issues like uneconomic size of holdings, low price of natural rubber and scarcity of tappers. This paper analyses the persisting issue of scarcity of rubber tappers in the sector.

Widening demand-supply gap

The first census of rubber tappers conducted by Rubber Board in 2013 enumerated 77,207 tappers in the smallholdings sector in Kerala. The estimated tappers requirement to tap the existing tappable area of 4,56,000 ha in Kerala in the smallholdings sector under different systems of tapping is presented in Table 1.

The census revealed that 13.7 per cent (10,577) tappers were under S/2 d1, 81.2 per cent (62,692) were under S/2 d2, 4.7 per cent (3629) under S/2 d3 and 0.4% (309) under various other low frequency tapping (LFT) systems in the smallholdings sector. By assuming a stand of 400 trees per tapping block, these tappers could tap only 1,49,011 ha regularly. This shows there exists huge demand-supply gap of tappers in the sector, resulting in large number of holdings either left untapped or tapped irregularly.

Inherent structural bottlenecks

In the general agricultural sector of Kerala, helpers of masons in the rural construction sector are considered to be the most immediate group with whom agricultural labourers identify or that these segments of rural labour markets interact during short-term fluctuations in the supply and demand. Similarly, supply of tappers at a given point of time is determined to a great extent by the wage income of tappers and the wage rates prevailing in the sectors closely interacted by the tappers in the smallholdings sector. Lower wage income of tappers in relation to wage of agricultural labour and semi-skilled workers was reported as the main reason for aversion of younger generation to tapping job. Trends in the wage rate of tappers in the smallholdings sector of Kerala are presented in Table 2.

Based on the structural breaks observed in the wage rate of rubber tappers since 1980, the entire period was sub-divided into five. During the entire time period, except for the period 2014 to 17, the wage rate of tappers has been increasing in real terms. The highest growth rate in nominal and real wages was observed during 2005 to 2013. A plateau in the growth of nominal wage rate was observed after 2013 and hence the real wage rate showed a decline (Fig 1).

Though wage rate of tappers has been showing growth in nominal and real terms till 2013, the sector has been facing severe scarcity of tappers. This shows that increasing wage rate has not succeeded in attracting sufficient tappers into the sector. Hence, wage share, which is a measure of distribution of income between the capital and labour, was computed to know the distribution of income between the farmers and tappers in the sector. Trends in wage share of rubber tappers in nominal and real terms are presented in Table 3.

The wage share of tappers has increased in the last one decade both in nominal and real terms. Though wage rate of tappers has declined in real terms in the last few years under analysis (Fig 1), wage share has been increasing in the smallholdings sector. Increasing wage share in the sector indicated better distribution of income among the capital and labour.

Nevertheless, the wage rate of tappers, both in nominal and real terms, has been increasing (except for the past a few years) and the sector exhibited an increasing wage share in real terms, the sector failed to attract sufficient tappers, leading to severe scarcity. This warrants for deeper analysis to understand the issue. Hence, a comparison of estimated wage incomes of rubber tappers with agricultural labourers and helpers of masons in the construction sector was done and presented in Table 4.

The estimated annual wage income of rubber tappers in the smallholdings sector of Kerala was found to be 44 per cent and 59 per cent less than their counterparts in the general agriculture and construction sectors respectively. This makes the sector less attractive for the potential new entrants, which is ultimately reflected in tappers supply. Due to division and fragmentation of rubber holdings, the average size of holdings has come down and number of trees available for tapping was only 286 trees per tapping day under single grower dependence system and 75 per cent of tappers in the sector were engaged in the single grower dependence system.

In piece rate-based wage payment system, number of trees tapped per day and number of tapping days per year determines the annual wage income of tappers. Thus, in the present scenario, the smallholdings are incapable of giving more tapping task to the tappers to enhance their wage income. Hence, prevalence of single grower dependence, small size of holdings, lesser number of trees available for tapping per tapping day and the piece rate-based wage payment are the bottlenecks in enhancing wage income of tappers. But, in their effort to retain experienced tappers in the milieu of tappers scarcity, the farmers were forced to follow the labour intensive high frequency tapping systems with more tapping days, though it has implications on net farm income.

Even though the tapping wage rate and wage share has been increasing in real terms, the tappers are expected to demand a hike in the wage rate as the wage income earned by them is substantially lower than their counterparts in other rural employment sectors. In the present scenario, to make wage income of tappers on par with that of agricultural labourers and helpers in the construction sector, a hike of 79 per cent and 143 per cent respectively is required in tapping wage rate (Table 5).

But, an increase of this magnitude in the wage rate is not feasible as further hike in the wage rate would seriously affect sustainability of rubber cultivation as with the present cost of cultivation and price of rubber, the farm income is declining in real terms (Fig. 2) and wage share is increasing (Table 3).

Limited options

Since labour is becoming costlier and farm income has been declining in real terms due to uncertain prices, the options available with smallholdings are either to shift to other profitable crops or adopt cost saving technologies including mechanization as tapping accounts for more than 80 per cent of the labour requirement in mature rubber plantations. Generally, mechanisation is done as a labour saving process that occurs due to the increasing scarcity of labour most often reflected in a rising wage rate. But, since the scope for mechanisation in rubber tapping is limited and adoption of cost saving low frequency tapping (LFT) is constrained by the small size of holdings, farmers may either prefer to keep their plantations untapped or shift to other profitable crops. At present, as per Rubber Board data, around 30 per cent of the mature plantations are left untapped in the smallholdings. This will have serious implications on the rubber smallholdings sector as majority of the farmers are small and marginal with average size of holdings of less than 0.5 ha. A study conducted by the Centre for Development Studies, Thiruvananthapuram, found that the net operating income from an acre of rubber cultivation is only Rs. 16,732 in Kottayam and Rs. 19,681 in Thiruvananthapuram, which is not adequate to induce the rubber growers to continue with rubber cultivation. It was also observed that the recorded net income of those with holding size below 2 ha and depending only on rubber cultivation for their livelihood will be below the poverty line.

Thus, declining profitability is expected to dissuade small growers in Kerala from rubber cultivation and encourage them to explore alternatives. This will have far reaching consequences in the sector as the share of part time farmers are already high and a recent survey by the Economics Division, RRII revealed that for 69 per cent of farmers in Central Kerala, income from rubber accounted for less than 50 per cent of the total household income.

Collapse of the smallholder’s rubber sector in Kerala will have serious impact on natural rubber production in India as the state contributes nearly 78 per cent of total natural rubber produced in the country and the smallholdings sector accounts for nearly 90 per cent of area and production in Kerala.

Collectivism to circumvent the structural bottlenecks

Earlier studies have suggested methods like crop sharing and production incentives with annual compensatory allowances as alternatives to overcome the hurdles inflicted by the piece rate-based wage payment system and low tapping task in enhancing wage income of tappers to attract more tappers into the sector. But, large scale adoptions of these propositions were not reported in Kerala. Crop sharing is not sustainable in the long run as the return to capital is marginal and hence would deter large scale adoption by the small and marginal farmers. Production incentives to match the wage income of tappers to that of labourers in the general agricultural sector and helpers in the construction sector (Table 4 and 5) would render rubber cultivation uneconomical due to high cost of production in the smallholdings, which has long lost its economies of scale.

Prevalence of single grower dependence, small size of holdings and lesser number of trees available for tapping per tapping day being the critical bottlenecks in enhancing wage income of tappers and attract new tappers into the sector, any new system adopted should be capable of negotiating these bottlenecks efficiently to ensure tappers flow into the sector. Division and fragmentation of holdings aggravates these bottlenecks and render rubber cultivation uneconomical. Thus, as a measure to overcome these bottlenecks, collectivism/co-operative farming is suggested as an alternative. Collectivism would help to circumvent these structural bottlenecks of the smallholdings viz., small size of holdings, lesser number of trees available for tapping and prevalence of single grower dependence of tappers, as in collective farming the factors of production are pooled and the farm is managed as a single unit on co-operative basis. Hence under collectivism tapping task and wage income of tappers could be enhanced considerably. Willing farmers in the smallholdings sector can be bought under different farmer’s co-operatives and the farm can be managed as a single unit by professional managers under the supervision of the elected members.

Collective management of small rubber holdings under co-operative/collective farming would facilitate large scale adoption of cost saving technologies like LFT, as the holding size barrier for its adoption could be overcome by collectivism. Since the farm management decisions are implemented uniformly across the units managed under collectivism, it will have the advantage of economies of scale. Though LFT is recommended as a cost saving strategy in mature plantations to make rubber cultivation profitable, its large-scale adoption is constrained by the small size of holdings in the smallholdings sector.

The first census of rubber tappers by Rubber Board in 2013 recorded its adoption as below 5 per cent in Kerala. By following the LFT (S/2 d7) under collective farming, the tapping task and employment of tappers could be enhanced further (Table 6) and the wage income of tappers could be equated with their counterparts in the rural labour market. Table 6 reveals that with the present tapping wage rate itself, the wage income of tappers could be equated with the income earned by their counterparts in the rural economy under collectivism. In addition to higher wage income, the tappers attached to farmer’s co-operatives would have better access to welfare schemes extended for the tappers by the Rubber Board as the first tappers census observed poor percolation of the welfare schemes among the tappers, since the tappers in the smallholdings were unorganized.

The proposed collective farming is different from the activities performed by the Rubber Producers Societies (RPS). The present day RPSs are basically involved in technology dissemination, provide different services like subsidized input distribution, collective processing and marketing of NR. A few RPSs and Rubber Board promoted trading companies are organizing tappers under tappers banks to tap holdings which are either untapped or abandoned due to absentee farmers, non-availability of tappers and declining profitability due to price crash. Though tappers attached to the tappers bank under the present system get higher remuneration than their counterparts in the smallholdings (Table 7), this will not ameliorate tappers scarcity and encourage large scale adoption of LFT in the sector, as the bottlenecks discussed earlier remains.

In the proposed collective farming, farmer’s co-operatives are expected to play a major and direct role in rubber production by pooling the factors of production (plantations). The authority to make farm decisions would be vested with the co-operatives rather than individual farmers and the profit shall be shared among the members.

Conclusion

Though wage rate and wage share has been increasing in real terms in the small holdings sector, the wage income of tappers were substantially lower than the wage income of labourers in the general agricultural sector and helpers in the construction sector with whom tappers in the smallholdings relate in the rural labour market. Due to presence of structural bottlenecks as such as smaller size of holdings, lesser number of tress available for tapping, piece rate wage payment system and prevalence of single grower dependence, the sector was incapacitated to augment wage income of the tappers to equate it with that of labourers in other rural sectors. To attract more tappers into the sector by increasing the wage income of tappers by circumventing the structural bottlenecks, collective farming under farmer’s co-operatives following the principles of collectivism is proposed. Collective management of plantations will not only help the tappers to get regular employment, sufficient tapping task and remunerative wage income, it would also have the added advantage of bring down the cost of production of NR and increasing profitability of NR cultivation as it would also facilitate large scale adoption of labour and cost saving technologies for rubber production.

Zeon And Yokohama Rubber Advance Sustainable Rubber Project With New Facility Completion

- By TT News

- August 04, 2026

Zeon Corporation has finalised the construction of a new bench-scale facility at its Tokuyama Plant in Shunan City, Yamaguchi Prefecture, dedicated to advancing the efficient production of butadiene from sustainable ethanol sources. The project, which broke ground in July 2025, represents a strategic move to establish a naphtha-independent raw material supply chain, thereby bolstering both corporate sustainability and the broader transition towards a carbon-neutral society. The facility is slated to commence full-scale operations in January 2027, with the ultimate goal of achieving commercial viability by 2034.

A commemorative ceremony took place at the plant site on 31 July 2026, drawing a total of 46 attendees. The gathering included official representatives from Japan’s Ministry of Economy, Trade and Industry (METI), the New Energy and Industrial Technology Development Organization (NEDO) and local governmental bodies from Yamaguchi Prefecture and Shunan City. Also present were delegates from the Yokohama Rubber Company, the construction contractor and various affiliated firms, alongside Zeon’s leadership, including Akira Honma, the Corporate Officer and Tokuyama Plant Manager.

This initiative forms one half of a dual-themed research and development programme undertaken in partnership with Yokohama Rubber, under the auspices of NEDO’s Green Innovation Fund. The collaborative effort is focused on the social implementation of technologies for synthesising both butadiene and isoprene from renewable biological materials by the 2030s. As part of this process, Zeon is set to produce a prototype polybutadiene rubber using the output from the new bench-scale facility, while Yokohama Rubber will subsequently manufacture test tyres from this material and conduct performance evaluations on test tracks.

Both companies have outlined a clear roadmap, intending to finalise the core technology for societal deployment by 2030 through the operation of a larger pilot plant, with full-scale commercialisation targeted for 2034. The bench-scale facility is a critical precursor in this phased approach, providing essential data for the scale-up process.

The broader project encompasses two selected NEDO themes, both subsidised through the Green Innovation Fund. The first involves the highly efficient synthesis of butadiene from ethanol, with technical cooperation from the National Institute of Advanced Industrial Science and Technology. The second focuses on biotechnological pathways to directly produce butadiene and isoprene from plant-based materials, involving partnerships with the Institute of Science Tokyo and RIKEN. Both tracks aim to supplement synthetic rubber feedstocks and support closed-loop recycling, aligning with Japan’s 2050 net-zero emissions goal by fostering long-term industrial innovation.

- Association of Natural Rubber Producing Countries

- ANRPC

- Monthly NR Statistical Report

- Natural Rubber

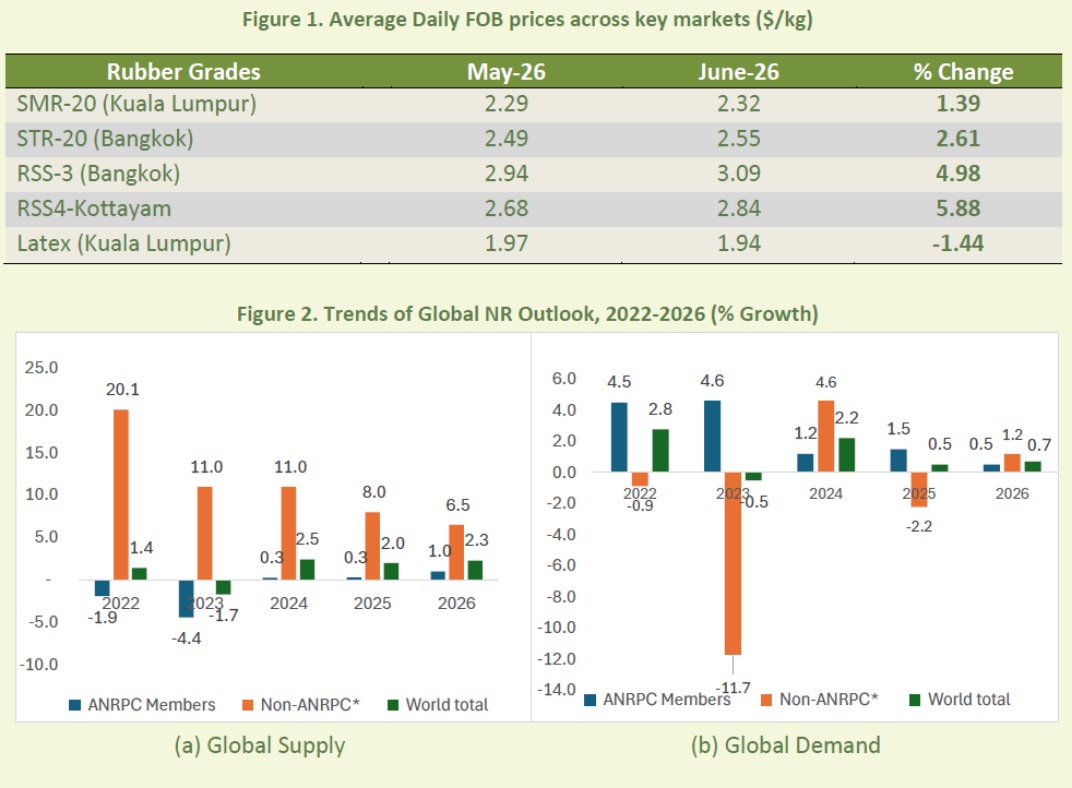

ANRPC Publishes Monthly NR Statistical Report For June 2026

- By TT News

- July 31, 2026

The Association of Natural Rubber Producing Countries (ANRPC) has released its Monthly Natural Rubber Statistical Report for June 2026, a month defined by price resilience amid conflicting market forces. The provisional reopening of the Strait of Hormuz triggered a sharp 20.29 percent drop in Brent crude oil prices to USD 85.40 per barrel. However, this bearish signal was counterbalanced by persistent supply constraints from El Niño-related weather disruptions across major producing regions.

Physical rubber prices posted broad-based gains across most grades. SMR-20 rose 1.39 percent to USD 2.32 per kilogramme, while STR-20 gained 2.61 percent to USD 2.55 per kilogramme. RSS-3 and RSS-4 advanced 4.98 percent and 5.88 percent to USD 3.09 and USD 2.84 per kilogramme, respectively, though latex eased 1.44 percent to USD 1.94 per kilogramme. On the trade front, China's imports surged 7.14 percent month-on-month, while India and Viet Nam declined. Export growth was recorded for Cambodia, Viet Nam and Indonesia, though Thai shipments contracted.

Global production for 2026 is projected at 15.310 million tonnes, up 2.3 percent from 2025, driven by gains in Thailand, China, India and Malaysia. However, June output fell 3.7 percent year-on-year to 1.207 million tonnes due to seasonal wintering and El Niño-related weather disruptions. Malaysia, Indonesia and Cambodia have introduced new incentive and governance measures to strengthen their sectors. Global consumption is forecast to grow 0.7 percent to 15.411 million tonnes in 2026, with June consumption rising 3.3 percent to 1.300 million tonnes, led by China and India amid steady tyre and EV-related demand.

Currency markets saw the Malaysian ringgit trade between RM3.96 and RM4.08 against the US dollar, while the Thai baht ranged from 32.56 to 33.24. In futures trading, the SHFE September 2026 contract averaged 17,580.68 CNY per tonne, down 0.45 percent month-on-month, while the SGX September contract averaged USD 2.24 per kilogramme, up 1.75 percent, with both reflecting tightening supply and firm downstream demand.

Pyrum Secures Long-Term Supply And Offtake Agreements With Pirelli

- By TT News

- July 31, 2026

Pyrum Innovations AG has finalised long-term supply and offtake agreements with Pirelli, reinforcing the tyre manufacturer’s European Tyre-to-Tyre initiative. The deal secures Pirelli’s purchase of Pyrum’s ThermoTireBlack (TTB) for use in its European production facilities, while Pirelli will provide Pyrum with end-of-life tyres from designated German sources.

These contracts simultaneously bolster Pyrum’s feedstock security and guarantee an industrial outlet for its recycled materials, covering both raw material procurement and product commercialisation. Through its proprietary thermolysis process, Pyrum transforms scrap tyres into ThermoTireBlack, which can substitute fossil-based carbon black, and ThermoTireOil (TTO), destined for chemical industry use. The partnership offers further validation of Pyrum’s technology within a certified European value chain involving tyre, chemical and synthetic-rubber leaders.

Pyrum also supports the broader Tyre-to-Tyre project, initiated by Pirelli with BASF and Synthos, which reintroduces secondary materials from used tyres and production waste into new tyre manufacturing via an ISCC PLUS-certified, traceable system.

Pascal Klein, CEO, Pyrum Innovations AG, said, “Signing these long-term agreements with Pirelli is an important commercial and strategic milestone for Pyrum. The coöperation secures both the supply of end-of-life tyres and an industrial outlet for our TTB. It confirms that our technology and products meet the requirements of one of the world’s leading tyre manufacturers and can contribute to the establishment of scalable circular value chains in Europe.”

MICHELIN ResiCare And IMCD Europe Forge Strategic Distribution Partnership For 5-HMF

- By TT News

- July 30, 2026

MICHELIN ResiCare, a specialist in renewable and high-performance chemical solutions, has entered into a distribution partnership with IMCD Europe, a major international distributor of speciality chemicals. The agreement centres on the European supply of 5-hydroxymethylfurfural (5-HMF), a bio-sourced compound produced at the company's Isère-based industrial facility in Péage-de-Roussillon.

Under the new arrangement, IMCD Europe will handle distribution across the continent while MICHELIN ResiCare maintains direct engagement with its key strategic accounts. The collaboration aims to significantly widen the molecule's availability to European manufacturers through an optimised logistics framework and localised technical support, thereby addressing rapidly growing demand within the materials and formulation chemical sectors.

The French production site, scheduled to begin operations in early 2027, will have an initial annual capacity of 3,000 metric tonnes. This domestic manufacturing capability represents a critical step in securing European access to a molecule deemed strategically important for the region's chemical industry, reducing reliance on external supply sources.

IMCD will contribute its technical expertise, market knowledge and pan-European distribution network to facilitate the integration of 5-HMF into new applications. The company's established footprint in polymers, advanced materials and speciality formulations positions it to provide developmental support to manufacturers exploring alternatives to fossil-derived intermediates. MICHELIN ResiCare has already spent two years assisting major industry players with application evaluations, and the partnership is expected to expand these efforts across a broader customer base.

Derived from fructose through non-toxic green chemistry and already REACH-registered, 5-HMF serves as a versatile building block for low-environmental-impact resins and can replace conventional petroleum-based ingredients across diverse industries including agriculture, cosmetics, construction, transport, aeronautics and electronics. The collaboration reinforces MICHELIN ResiCare's commitment to renewable resources and sustainable material development while aligning with IMCD's dedication to advancing innovation in greener chemistry solutions.

Laurent Lemonnier, CEO, MICHELIN ResiCare, said, “This partnership with IMCD represents a major step forward in our desire to popularise the use of 5-HMF and to support the transition to a more responsible chemistry. With its technical expertise, its capacity to support customers and its European location, IMCD is the perfect partner to speed up the distribution of this molecule of the future.”

Comments (0)

ADD COMMENT