Certainty With Certified Rubber

- By Juili Eklahare & Gaurav Nandi

- August 23, 2022

Rubber certainly has its role to play in forest landscapes across the world, with natural rubber plantations having risen as a substantial basis of deforestation. One element that addresses deforestation concerns is the correct certification of rubber – be it natural or synthetic. International Sustainability & Carbon Certification (ISCC), a globally leading certification system, works with the objective of providing sustainability solutions for fully traceable and deforestation-free supply chains, inter alia involving the rubber industry. ISCC was one of the presenters at the Tire Technology Expo 2022 at Hannover, Germany, and Dr Jan M Henke, Director, ISCC, threw light on the nitty-gritty of certifications in the rubber industry, their clients in the tyre and rubber industry and more, in an interaction with Tyre Trends.

Can you tell us about your global sustainability scheme?

Our global sustainability and carbon certification scheme has certified companies in more than 100 countries. We certify entire supply chains from farms to plantations and forestry, and also the point of origin of waste and residues, biogenic and fossil waste. This is also covering rubber and natural rubber. Moreover, we cover biogenic waste and residues, including fossil waste, like carbon black, which is, again, used in the rubber industry. We also certify pyrolysis, where recycled mixed plastic waste can help produce synthetic rubber out of the pyrolysis oil. And we certify the entire supply chain, sustainability of raw material.

What is Meo’s role?

Meo initiated ISCC in a multi-stakeholder process a long time ago. It once was a Meo project and went on to become an operations and certification scheme. It was even recognised by the European Commission and some other authorities. It later got segregated from Meo, and ISCC is governed by the ISCC Association with more than 200 members.

So, what role does Meo play in this in case of certification?

Certification is always by independent, third-party certification bodies. ISCC is the standard development. Today’s ISCC was once a project of Meo. It then went on to become independent and operational, and was no longer a project but an individual entity running and further developing and improving the certification scheme.

The operations of the certification system, database, registration, qualification, training programme, integrity programme, the website and all the day-to-day business is done by ISCC. We are currently incorporating 45 certification bodies that are actually doing the on-site audits based on the ISCC standard.

Is ISCC recognised by the European Union?

Yes, it is being used in many sectors, like in bio energy, bio fuel, renewable transport fuels etc. In fact, ISCC is also recognised by the European Commission and by companies based on their sustainability standards and different industry initiatives.

Hence, ISCC is active on a really broad scale, covering different types of raw materials, natural rubber being one of them. We are also covering waste and residues for pyrolysis and their outputs. We then go to all the different end markets, which can be polymers, rubber, tyres, packaging, all types of plastic products, bio energy or any type of renewable fuels, aviation fuels, maritime fuels etc. This is global and is being used in more than 100 countries.

Tyre companies are talking about sustainability, but the larger part of the industry is of small stakeholders, especially in the natural rubber segment, where traceability and accountability are the main issues. How do you see this?

That’s a big challenge, especially in rubber production. At the cultivation level, there are a lot of small holders. There also exist large plantations that are easier to implement and certify. However, it’s definitely a bigger challenge with the small holders; it always depends on how well they are organised, whether there are certain structures, cooperatives or some central units.

Can you tell us about the certification of natural rubber?

The certification of natural rubber is definitely possible. Palm oil is maybe another example where the setup is quite similar sometimes. Also, with respect to the small holders, sometimes the companies are the same. Furthermore, we are very active in the palm oil sector with ISCC. We now also see a demand for natural rubber sustainability certification.

Is there a different process for getting certified in the rubber industry or is it a standard process?

It’s a standard process. It works on plantation. In fact, it works more or less the same as for palm plantations. But you certainly need to make sure that all the small holders reach a certain level, which is difficult. So starting out, bigger plantations may be easier because it’s easier for them to properly prepare for the certification audits. And then, you need to involve more farmers, step by step.

Who decides the standard process to get the certifications?

ISCC develops the standards and the requirements in the multi-stakeholder process. It then comes down to a company saying that it wants to become certified, use ISCC and also make certain claims and communications to its customers and stakeholders. They then reach out to a certification body, that is cooperating with ISCC. Following this, the certification body will do the audit on site – the third-party auditor will also make a decision on the issuance of the certificate.

Can tyre manufacturers get different certifications? For instance, one for natural rubber and another one for synthetic rubber? Or do they get one for all?

If tyre manufacturers source raw material for manufacturing from natural rubber but also synthetic rubber and everything under ISCC, then it’s one audit. Then the auditor would look into aspects of the volume of natural rubber being used that has been certified, although upstream. If one buys from certified suppliers and if the same auditors check, then aspects like the share of the certified synthetic rubber being used, the share of carbon black, etc. are taken into account. And finally, everything can be put together and a certain claim can be made.

Can tyre companies get a separate certificate for natural rubber?

Yes, they can. They can have separate certificates for natural and synthetic rubber both, or even of everything together. As for the final tyre, let’s say, if it’s 20 percent natural rubber and 20 percent synthetic rubber (40 percent of the tyre), then they can make certain sustainability claims on use of sustainable, circular materials etc.

What is the value of a certification?

It’s no deforestation – that’s key when it comes to natural rubber. When you certify, ‘no deforestation’ is the core requirement and deforestation is not allowed under ISCC. It is about additional environmental and social human rights criteria. This fits fine in this part of ISCC’s sustainability standard. And then it’s certainly about traceability in the supply chain, all the way in the end to the final tyre. And if this is established, then you can certainly make claims about the rubber or the final tyre, saying that it has been sustainably produced, based on sustainably sourced raw materials etc.

Plus, if you do this in a smart way, then you can actually cover the natural and synthetic rubber. Natural rubber and synthetic rubber are both very important parts of the final tyre. Both can be covered under ISCC.

Deforestation is a big issue, mainly in Southeast Asian and African countries. How difficult is it to keep an eye on that?

It’s not always easy to handle. Deforestation is not allowed under ISCC; there is a cut-off date of January 2008. If there was deforestation after January 2008, one cannot become certified. However, replanting or a change from palm to rubber is not considered as deforestation.

For example, if you have a palm plantation and if you cut it and plant rubber after 25 years, then that’s not deforestation. That’s just normal replanting.

Also, ISCC is certainly doing assessments, supported by remote sensing. Our core principle is no deforestation, which is very important to ISCC and its stakeholders. ISCC is not just us doing the operations in Cologne; there’s the ISCC Association for the multi-stakeholder dialogue. It has over 200 members from entire supply chains, industries, plantation companies, mineral oil, chemical companies, converters etc. We also have research organisations from different regions involved. In fact, also a number of non-governmental organisations are members of the ISCC Association.

The association meets annually and makes important strategic decisions and elects the ISCC Board. Due to the representation of the research sector and non-governmental organisations, there is quite a good balance of what people want and further development.

Can you tell us about the commercial benefits involved in having a certification?

There is a big value in it. It reduces sustainability risks for companies, helps to establish monitoring, protects the license to operate and has commercial value. For example, the OEMs ask for more sustainable products or lower greenhouse gas emissions. They all have climate neutrality commitments in place and need to start delivering step-by-step now; they need to show what are the activities that they are engaged in and how those improve sustainability in the overall supply chain. Here, ISCC certification can be used.

How do you maintain transparency in certification as a third party?

There is an annual audit. The certificate is valid for one year and then there is a re-certification. The company needs to provide evidence in every re-certification that the rules are being followed. And if they are not, a renewal of the certificates is not possible.

We certainly have quality management and training for companies and the auditors as well, who conduct on-site audits. What’s more, we have our own integrity programmes, where we send out our own auditors. These auditors work for ISCC and double-check the performance of the companies and the work of third-party auditors. Therefore, this integrity programme is key. We have the website where all the certificates are being published and the entire standard is public.

Do you help companies improve their sustainability supply chain?

No, we don’t consult. At ISCC, we are not involved in supporting the companies in order to improve. We have the standard and we conduct the training for companies. The preparation for the audit is not where ISCC is involved; it’s independent from that type of work. And the certification bodies are not allowed to consult in parallel either. ISCC is the independent standard that is used to certify that companies fulfil the sustainability requirements.

What are the other segments that you cover in the tyre industry?

It’s the entire supply chain. Petrochemical industries, tyre manufacturers etc. can all be covered. This also includes everything from plantations to the end product in the tyre industry.

Which is the easiest and the toughest one to certify?

All elements of the supply chain need to be covered.

This can sometimes be a challenge in the beginning, so as to convince your suppliers and also get certified. But, in truth, we have more than 6,000 certificates under ISCC. So there are already a lot of players that have valid certificates, and now this is starting to move into the space of rubber and tyre manufacturers.

Can you tell us about your clients in the rubber and tyre industry?

We have requests from many tyre producers right now. Some producers are certified already. Plus, we have requests for carbon black and first requests for natural rubber. We see the number of requests increasing, and we do have first certificates and first registrations from tyre producers. So we expect this to rise further as the industry needs to show compliance with their sustainability and climate neutrality commitments.

We see the entire tyre industry now targeting sustainability. So how do you find more opportunities and what’s your plan to get more client support?

ISCC started to get really further engaged in the rubber and tyre industry about a year ago; the industry has started understanding the standards, participating in ISCC trainings, joining our stakeholder events etc. Therefore, step by step, they got to know ISCC better and what it could do for them. They have now even started to get involved and do certifications, including reaching out all the way to the cultivation of natural rubber.

Are you going to focus on the Asian market?

Yes. In fact, we already have a few hundred certificates in Malaysia, Indonesia and other countries in the region. These markets are truly important. Our other key markets are North America and Europe, while we are also active in Africa and South America.

We are, eventually, trying to do more and convince people to become certified, show compliance to sustainability requirements, engage in a continuous improvement approach to become more sustainable and then allow manufacturers to really make claims.

JK Tyre Raises Product Prices Amid Raw Material Surge

- By Sharad Matade

- August 11, 2026

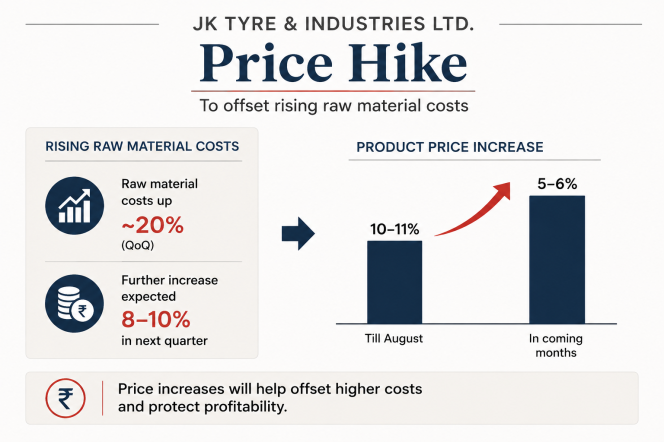

JK Tyre & Industries has increased product prices and signalled further hikes as it seeks to offset rising raw material costs, even as demand remains resilient across segments.

The company said raw material prices rose about 20 percent quarter on quarter, with a further 8–10 percent increase expected in the following quarter. The increase has put pressure on margins, given that about 70 percent of tyre industry inputs are petro-based.

In response, JK Tyre raised product prices by 10–11 percent until August and plans an additional increase of 5–6 percent in the coming months to mitigate cost pressures.

The pricing action comes despite steady demand conditions. The company reported a 25 percent year-on-year increase in domestic volumes in the June quarter, supported by growth across both replacement and original equipment manufacturer segments.

Management indicated that demand remained stable across commercial vehicles, passenger vehicles and two- and three-wheelers, with no significant production cuts from OEM customers.

The company also said it continues to focus on premiumisation, with higher-margin products such as 16-inch and above passenger car tyres increasing their share in the sales mix.

Yokohama Rubber H1 Profit Soars More than Double And Raises Full-Year Outlook

- By Sharad Matade

- August 11, 2026

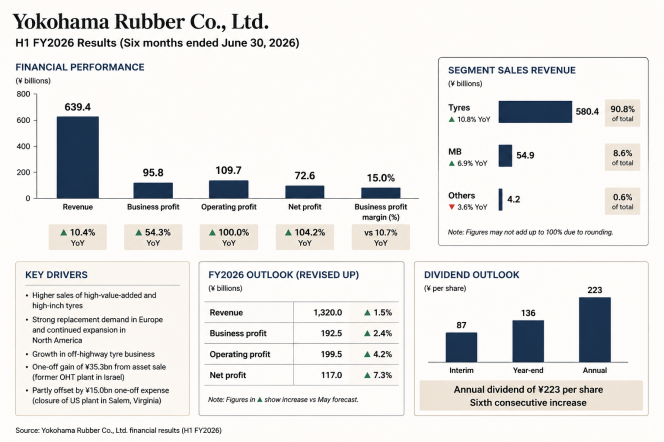

Yokohama Rubber reported record earnings for the first half of fiscal 2026, with profits more than doubling and margins reaching a historic high.

The Japanese tyre maker said sales revenue rose 10.4 percent year on year to ¥639.4 billion in the six months to June, while business profit increased 54.3 percent to ¥95.8 billion. Operating profit doubled to ¥109.7 billion, and profit attributable to owners of the parent rose 104.2 percent to ¥72.6 billion.

Business profit margin improved to 15.0 percent, compared with 10.7 percent a year earlier, marking a record level for the company.

Yokohama Rubber said the results reflected strong performance across its businesses, delivering record first-half highs in all key earnings categories.

Segment data showed that tyre sales revenue rose 10.8 percent year on year to ¥580.4 billion, accounting for 90.8 percent of total revenue, while the MB (Multiple Businesses) segment recorded revenue of ¥54.9, up 6.9 percent and contributing 8.6 percent of the total. Other businesses declined 3.6 percent to ¥4.2 billion.

Business profit growth was led by the tyre segment, where profit increased 57.3 percent to ¥89 billion. The MB segment posted profit of ¥6.3 billion, up 22.5 percent, while other businesses reported profit of ¥0.5 billion.

The company said tyre segment growth was supported by higher sales of high-value-added and high-inch tyres, as well as increased volumes in the off-highway tyre business. Replacement tyre demand strengthened across regions, with strong sales in Europe and continued expansion in North America.

Operating profit was also supported by a ¥35.3 billion gain on the sale of assets at a former off-highway tyre plant in Israel, partly offset by a one-off expense of ¥15.0 billion related to the closure of a US tyre plant in Salem, Virginia.

The company also revised upwards its full-year forecast for fiscal 2026. It now expects sales revenue of ¥1,320 billion, business profit of ¥192.5 billion, operating profit of ¥199.5 billion and profit attributable to owners of the parent of ¥117 billion.

JK Tyre Reports Steady Quarterly Revenue As Margins Face Pressure

- By TT News

- August 10, 2026

JK Tyre & Industries reported broadly steady revenue for the first quarter of the financial year, with profitability constrained by higher input costs.

The company posted consolidated revenue of INR 39.56 billion for the quarter ended 30th June, 2026, while earnings before interest, tax, depreciation and amortisation (EBITDA) stood at INR 2.68 billion, implying a margin of 6.8 percent. Profit before tax was INR 0.54 billion and profit after tax came in at INR 0.43 billion.

According to the company’s financial statement, revenue from operations was INR 39.46 billion, compared with INR 38.69 billion in the corresponding period a year earlier.

Operating profit declined to INR 2.68 billion from INR 4.24 billionn a year earlier, reflecting pressure on margins.

Dr Raghupati Singhania, Chairman and Managing Director, said: “JK Tyre continued its steady performance in Q1FY27 with a consolidated turnover of INR 3.56 billion, supported by strong demand momentum across segments. The performance is driven by sharp focus on customer centricity, product excellence and disciplined execution across markets. During the quarter domestic volumes grew by 25 percent on year-on-year basis, across both replacement (12%) and OE markets (42%), with increasing contribution from higher-value added products. The continuing west Asis crisis led to a sharp increase in raw material prices which impacted our gross and operating margins. As is known approximately 70 percent of the tyre industry raw materials are petro based, hence, it is highly vulnerable to oil price movement”.

He added: “With a sharper focus on operating leverage, cost reductions, and increasing share of premium products, JK Tyre remains confident to improve performance in FY27 with double-digit revenue growth, aiming to create enduring value for all stakeholders with an increased profitability through strategic expansions”.

Dunlop And Beta Motorcycles Strengthen OE Ties With New Geomax Tyre Lineup

- By TT News

- August 08, 2026

Dunlop Motorcycle Europe has expanded its original equipment partnership with Beta Motorcycles, securing a deal to supply advanced Geomax tyres across the Italian brand’s trial and motocross lineups. The enhanced collaboration introduces new standard fitments for both competition disciplines.

For trial applications, the Geomax TL01 replaces the previous D803GP on Beta’s Evo and Sincro models. Engineered with a high-adhesion compound and a specialised block layout for angled terrain, the ultra-sticky tyre has already proven popular among Beta racers and now becomes factory-standard equipment.

In the motocross sector, Beta has adopted the Geomax MX34 for its entire RX range, covering both two-stroke and four-stroke 250 cc and 350 cc variants, as well as the 450 cc model. Designed primarily for intermediate ground, the versatile MX34 performs effectively across diverse surfaces, from soft mud to compacted dirt.

Donato Miglio, Race Team Manager Trial, Beta Motorcycles, said, "Geomax TL01 represents a significant step forward in performance, which is why we decided to adopt it as our original equipment trial tyre. Many of our riders already use it in competition, where it has proven its exceptional grip, stability and handling.”

Fabrizio Dini, Race Team Manager Motocross and Enduro, Beta Motorcycles, said, “In motocross, the latest generation of Dunlop MX tyres features significant performance improvements. Geomax MX34 provides excellent grip, particularly on dry surfaces, giving riders a reassuring feeling of safety and constant control. Both tyres suit our bikes perfectly.”

Miguel Morais, Original Equipment Manager, Dunlop Motorcycle Europe, said, “We are proud to deepen our partnership with Beta through the introduction of Geomax TL01 and MX34 across its latest trial and motocross models. Fitments like these are a strong endorsement of the capabilities of tyres throughout our range, and we’re excited that more and more riders will experience increased confidence and performance that helps them get the most out of their Beta motorcycles from their first ride.”

Comments (0)

ADD COMMENT