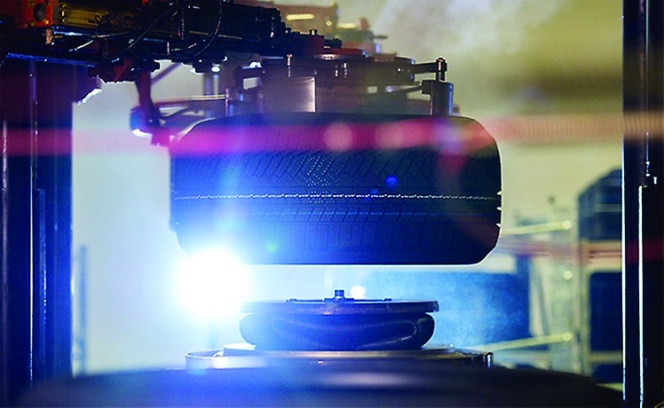

How To Get Maximum Benefit From Tyres: Commercial Fleet And Mining Operations

- By Ahmad Hidayat

- September 30, 2024

In human mobility, tyres are ‘the only contact between the vehicle and road’, to make people move from one point to another ‘safely’.

In land cargo transportation, they are the ‘work horse’ of the supply chain for any goods, whether industrial (raw material) or finished goods. In special applications such as mining, they are ‘mimicking’ pipelines in the oil and gas industry, such as piping where hydraulic pumps replaced by truck engines.

So tyres play a ‘critical role’ in transporting almost anything: ‘people and goods’ when we must deliver on land transport mode.

The challenges: Too many options

Its vital role is not questionable. But having that critical role doesn’t mean it’s easy to handle for the end user.

Why?

In the case of tyres, we know premium brands, regional brands and sometimes local brands. The classic question is: which one is the best?

For personal purposes (PCR), a decision could be made easily with the risk of losing a small amount of money. Simply fitting a tyre according to OEM standards will not be a big issue. The problem arises with fleet companies (trucking or bus) with tens, hundreds or even thousands of units of equipment.

Even riskier when it comes to OTR tyres, where prices can reach tens of dollars or more. It is not easy to pick which one is the best.

How to choose the most suitable tyre for operations?

In order to get the right choice, we must do the following:

1. Define performance indicators: Productivity or efficiency - Regarding commercial tyres (TB/AG/OTR/IND), performance is defined as productivity and efficiency. These two elements are sometimes aligned and sometimes contradictory.

Which one should be chosen?

It depends on the company’s goal or situation. We must optimise between those two so that it becomes ‘business decision’ and not a solely ‘tyre technical decision’. When productivity takes the lead compared to efficiency

One fleet of 120T giant trucks fitted with 27.00R49 has limitations due to the TKPH caused mainly by long distances, so the real site TKPH is quite high. It limits trucks operating cycles to only 6.5 per shift. It is only transporting coal at 120 T/cycle x 6 cycles = 720 T per shift, while the end user burns fuel without getting tonnage in return for a half cycle.

In this situation, the end user is not sensitive to efficiency; they are more sensitive to how to increase productivity.

When efficiency becomes the driver instead of productivity

The other situation is that coal transporters have problems with tyre costs due to inefficient tyre usage. The end user thinks they made a good choice using the 12.00R24 *** (three-star) rating. They expect a long life, but the outcome is the opposite. Testing was done with bias tyres (12.00-24), 18PR and 20PR. Comparison testing was done for six months, and in the end, we concluded bias tyres were more efficient than radial tyres.

The explanation for why bias tyres perform better than radial tyres comes from a pressure check done with 1,500 points of data show ‘intentional’ pressure reduction.

When it was discussed with site management and the driver, the driver told management that the hauling road was undulating, forcing them to reduce pressure. If they don’t reduce pressure, they will suffer from back pain.

So in terms of truck load, it is not overload, but in terms of tyres, it becomes overload due to low pressure. As bias tyres use nylon as the carcass, they have more resistance to fatigue, whereas radial tyres using steel cord have less resistance to fatigue and are more prone to premature failure.

The common sayings that radial is better than bias, premium is better than normal brand and thicker tread is better than shallow tread are more myths than realities. It all depends on the requirements coming from the field/ operations.

2. Optimise tyre life

The only way to do this is the end user doing an assessment of their requirements for each application, operating condition and site/road condition. This way, they could be able to build up the tyre requirements and externalise their requirement to get the most suitable tyre specification from whichever brand and whichever type of tyres.

With tyre OEMs mostly developing products for the most common applications, the potential performance is not necessarily the best performance on every site, independent of the brand, tyre type etc.

The best suggestion for the end user and OEMs

OEMs should start Co-Creation Value by having close communication from the beginning about actual customer requirements and focusing on creating the most suitable solution rather than the most common approach.

How it becomes practical If fleet truck customers have more than 1,000 trucks and mining customers have at least 100 giant trucks, they would like to have the most suitable product rather than the most common product for their application, as their tyre cost will be significant to gain their attention.

Meanwhile, for OEMs, it is worth to develop tyres with the most suitable solution and treat the customer as Key Account.

How to measure the benefits for each party

For the end user, the more suitable the tyre, the more optimum tyre performance they will have. For OEMs, the measurement is quite simple: calculating the potential life-time value (LTV) of a customer (estimate revenue generated from this customer) compared to the cost-time value (CTV) of the customer (the spending on developing products and maintaining relationship with the customer).

And if LTV/CTV > 1, it is an Attractive Customer. If the estimated LTV/CTV is not attractive enough to be handled, the OEM could focus on another customer.

Summary

- Tyre optimisation for end-user applications is a fair measure, and the actual performance indicator aligns with the temporary business objectives of the end-user that could change over time; one time it will be more productivity focused, the other time it may be efficiency focus.

- Democratisation and an open field for the whole OEM player that is not dogmatised as premium always being better, radial always being better or star rating always being better. It is merely how end-users could define their operational requirements and work together as cocreators with certain OEMs.

- It is not necessary for OEMs to chase all market segments; each OEM could choose where they will be more competitive than others. Meanwhile, for the end-user, they will get high-quality and reliable service from certain OEMs on their tyre usage.

Representational image courtesy: cebmumbai/Facebook

The author is an engineering expert in the mining and truck tyres field.

The column was first published in August-September 2023 issue of Tyre Trends.

I can still vividly remember a journey I made in 1995 with my young Kenyan MD (who is no longer living) in a hired car from the Delhi Airport to some town close to Ludhiana to meet a tyre moulding machinery supplier. The travel was through vast expanses of paddy fields extending to miles, and in between, we could see large industrial sites far away. A clear sign of industry and agriculture co-existing synergistically. When passing the area called Kurukshetra, the driver mentioned that there was a war at this area a long time ago. He was obviously referring to the great war of the epic Mahabharata, a subject which still generates ample curiosity in me even at this advanced age. With growing years of maturity, I am more convinced that the great war symbolically and semantically depicts the inner conflicts going on in our own minds, while these are conventionally polarized as ‘black and white’ under the ‘all- or- nothing’ principle, and Kurukshetra represents our own hearts and intellect, commonly called the emotional brain and intellectual brain in today’s jargon. Equipped with my industry experience acquired for nearly six decades, I am tempted to make a rather feeble effort to understand what has changed in the managerial mind map over the past 50 odd years. It would be similar to finding parallels between the Vietnam War in the late sixties and current war going on in the Middle East, despite the common factor, US.

Quite in contrast to machinery and materials, the man component of the traditional 4Ms is the most confusing area despite the vast research that has been carried out over the years. It is said that the adult human brain consists of about 86 billion neurons, an astronomically high figure compared to memory capacity of the modern computers. Over the past few decades, the modern managerial mindset has undergone profound transformations. Managers today, particularly in the age group of 35 to 50 ( Gen X), operate in an astonishingly different scenario compared their counterparts 50 years ago. The two eras are fundamentally different and attempting to compare them is largely futile. The rapid changes, technologically, culturally, socially and psychologically, are so vast that today’s managers are shaped by globalisation, digitalisation and fierce competition, which has significantly altered their cognition, thinking patterns, values and behavioural approaches.

While most living managers of the older generation adopt a stance of lamenting about the ‘’good old times’, I think it would be more prudent to understand the realities of change. Management philosophies have undergone profound change, evolving from Taylor’s scientific management and Fayol’s top-down framework based on five key managerial functions to the humanistic approaches advanced by Carl Rogers and Maslow. This is the universal feature of impermanence of all conditioned phenomena (cause-effect related), discovered more than 2,600 years ago by Lord Buddha and some Greek and other Eastern philosophers. Endeavoring to maintain stability, in an ever-changing world scenario, has been the driver for the emergence of management concepts and theories, including the latest approaches seen in the contemporary modern world. Comparing modern managers with those from 50 years ago is unrealistic because of the complete change in the context. Earlier managers operated in stable and localised economies, while modern managers operate in a dynamic globalised environment. It is sometimes said that ‘when the President of the United Sates sneezes, the Eastern leaders catch a cold’, a fact amply demonstrated by the recent events.

Decision-making in the past was slow and experience-based, while today it is data driven, rapid and technologically assisted. Traditional management emphasised relationships, loyalty and progressive and gradual growth, while modern systems emphasise on performance metrics and quick results, like the instant coffee.

The growing corporate trends due to industrialisation over the past 30 years especially has witnessed increased focus on productivity, efficiency and outputs along with standardisation, which has made workers and managers becoming a part of a mechanised system. Modern corporate managerial thinking is also been heavily influenced by globalisation, due to exposure to international competition and the need to adapt to diverse cultures and markets and the pressures to meet global benchmarks and standards. The constrains and the stresses imposed on countries such as Sri Lanka is tough in these areas. A good example is the EUDR requirements, which initially was a nightmare to the rubber product manufacturing companies. A far more serious non-technical consequence is that the concept of a ‘global village’ is eroding values of the strong cultural and ethical foundation, leading to identity dilution among managers

During my association with the industry, particularly over the past 20 years, I have personally witnessed decline of the traditional values in the modern managerial mindset. This is also seen in some professional associations in which I have been a member for a long time. Some of the key trends noted are as follows:

a) Limited understanding and low priority given for religion, history and cultural heritage.

b) Reduced emphasis on ethics, empathy and social responsibility despite the fact that this has become a ‘catch word’ in most corporate circles.

c) Over reliance on technical knowledge and digital skills.

d) Decline in the respect for elders and their experience (crystallised knowledge)

e) Over confidence due to access to information, which brings forth a ‘know it all ‘stance.

f) Diminished openness to learn from others.

g) Difficulty in accepting criticism and feedback

While these tendencies directly affect workplace relationships, team cohesion and leadership effectives, the hidden or latent consequences have more deeper implications on personal and social wellbeing.

The Buddha in one of the discourses has observed that a person can victoriously face a battle against an army of elephants, horses, chariots and infantry by having the necessary resources, but it will be more difficult to win the war within due to mental conflicts.

Most business environments are characterised by aggressive target setting, continuous performance evaluations and competitive organisational cultures, which has caught the managers in a perpetual rat-race where success is narrowly defined by targets and profits while there is hardly any time for reflection or personal growth. This creates a certain emptiness and dissatisfaction even among the high achievers.

I find it interesting at this juncture to refer to the historic concept of Sigmond Freud (considered as the founder of Psychoanalysis), the structural components of the mind, namely Id (pleasure principle or gratification), Ego (reality principle) and the Super Ego (ethical and moral conscience). In order to minimise the negative impacts of the conflicts between them, the Ego resorts to defence mechanisms, or temporary coping solutions. Some of these are denial of the problem, repression of the feelings, projection of the blame to somewhere else and rationalisation or giving logical but false explanations. While these are useful in the short term, over reliance can interfere with mental functioning and emotional growth. All of us are unconsciously resorting to one or several of these in times of emotional turmoil.

The pressures of modern management have led to an exponential growth in mental health challenges in recent years, which include common mental disorders such as stress, anxiety, burnout, depression and features associated with Borderline Personality traits (emotional instability and impulsivity), which result in work-life imbalance and chronic dissatisfaction.

Due to the high psychological demands, there is a growing need for career and workplace counselling. Counselling is a relatively new term that came into prominence around the mid-20th century, before which guidance and support was traditionally provided by the religious institutions, parents, teachers and the elders in the society. Over the recent years, counselling has evolved as a unique profession. Many organisations, especially the larger ones due to the seriousness and gravity of the problems they experience, have established counselling as a regular activity performed in-house or outsourced. Counselling helps managers to cope up with stress and expectations, supporting emotional regulation and resilience and enhancing self-awareness and interpersonal skills, which results in reconnecting purpose and meaning and balancing professional and personal life to develop a healthier mind set. The modern managers must endeavour to have a balanced mind set which is an integrated mix of technical competence, human values, cultural awareness and emotional intelligence and wellbeing. Only then they can move beyond being mere ‘cogs in a wheel’ and become holistic, effective and ethical leaders in the modern world

It is somewhat ironic that Human Resource Sustainability is not named as a single standalone goal in the United Nations Sustainable Development Goals (SDGs) but covered under several headings such as Good Health and Wellbeing, Quality Education, Gender Equality, Decent Work, Economic Growth and Reduced Inequalities.

While I do not have firsthand information on how human resource counselling is caried out in other countries, my observations and experience in Sri Lanka is that it is done more in a fire fighting or reactive mode, where corrective and remedial measures are taken only in cases of psychological deviances. It is somewhat surprising because Sri Lanka is famous for its preventative public health care in pre and postnatal maternity health and school dental health. Industry safety and health is fairly well addressed in most large, medium and some small enterprises, although these are mainly covering the operational levels. Currently, several standard stress, anxiety and depression measuring scales, both qualitative and quantitative, are available, but they do not seem to be used proactively to detect the cinders underneath the ash. People in emotional distress invariably need to vent their thought and emotions, which causes several cognitive distortions and mental disorders. Active and empathetic listening plays the major role in a therapeutic counselling relationship

Coming back to the Mahabharata, the classic instance of counselling for a person in deep emotional conflict and inner war is the Bhagwat Gita, and all of us will need Lord Krishnas in different disguises at some stages in our lifetimes.

It is interesting how Buddha has adopted an integrative approach to the four aspects or components of wellbeing for human progress as:

- Physical wellbeing

- Mental wellbeing

- Social wellbeing

- Spiritual wellbeing

The author is a Management Counsellor from Sri Lanka.

Training: what does it mean and what does it entail?

- By Adam Gosling

- July 03, 2026

At the end of my career, I am at the return-on-investment stage, giving back my mentors’ investments in me for all those years ago, and even not so long ago.

Training to me is setting the standards that you wish your trainees to achieve. All those mistakes you learned the hard way, the tricks of the trade, the missteps can all be related to those who’ve chosen our industry. Help them understand how to learn.

The standard for training has to be set very high; no use having a low bar and then complaining that no one knows what they are doing. If you jump for the stars but don’t quite make it, then at least you’ve cleared the tree tops.

When setting training qualifications, the quality of the parameters of the applied learnings has to be not only high but sound. The written materials have to be water tight, the methodology without flaw and the evidence of successful learnings not just a tick and flick exercise. The candidates undertaking the training have to be assessed and then critically deemed competent.

One could be forgiven for not wanting to get on a commercial aircraft if the pilot had ‘purchased’ the qualification instead of working for years towards it; likewise, think about a surgeon operating. The methodology and learning materials have to be sound and qualified.

Bureaucrats often outline training without any real knowledge of what the industry involves. Sure, there are governmental outlines as to what has to appear and how it must appear, but does this really meet the requirements of industry? Few industries are so alike that the same template of learnings can be applied, but for the sake of being able to tick the boxes and say, ‘Yes Minister’, we have standardised learnings regardless of the actual industry requirements.

Safety is the paramount learning. There is no return on investment if the training candidate is injured or maimed and cannot actually perform the work they were trained in. There are only poor outcomes for all involved, from the employer to the family; the provided training must embed safety as a paramount requirement.

I acknowledge the human failings whereby, even with all safety systems engaged, poor judgements and flawed decision-making can lead to inauspicious outcomes. Humans are fallible creatures, and that is what makes us different from machines.

When engaged in a training process, all the ‘what ifs’ have to be considered. In the early days of my education in computing using pencils and card readers, I soon learned the base rule of garbage in equals garbage out, or GIGO. After numerous hours of hairpulling, a comma was identified as the error; it should have been a full stop. There were no error messages generated, no one looking over my shoulder assisting; I blundered on until I stumbled over the fact that I had screwed up. The outcome was negligible, just some lost time. For others in our industry, a mistake may mean the end of their career, loss of amenity and even loss of their life. Do we permit such ‘what ifs’ to be ignored in training?

In the early days of tyre service personnel training, I’d commence the session by telling the candidates ‘never use your first chance, you may not get a second’, then run a series of videos showing catastrophic tyre failures, some simple others disturbing, but the message was clear. There is a process that has to be followed; do not take short cuts and do not deviate without understanding the risks involved deeply and clearly.

In preparing training materials, the risks (regardless of industry) have to be clearly understood; there is no tolerance for a lack of risk assessment and associated mitigation. If a poor standard of materials is presented to newbies to the industry, how are they equipped to identify the flaws that could propagate the catastrophic outcomes we all seek to avoid?

Training is not unlike the manufacturing of a tyre. The materials involved in the construction have to be of sound quality; the processes used in the matrix of the materials to produce the end result we know as a tyre have to be exacting. Anything less and the end product is a blemish or down grade.

Is this what we desire in the personnel we train?

Tyre servicing is one of the most hazardous occupations that is not licensed. Electricians, medical workers, lawyers, all require strict licensing. Yet the personnel that manipulate large tyres that have destructive burst forces that can, and do, result in fatal injuries may not even be required to demonstrate their competency in the aspects of the duties they may encounter.

Tyres are ubiquitous in our societies; just as we observe with the current petroleum shocks, the loss of tyres would be just as disruptive to our modern way of life. We can live without social media (as much as the squeals I hear saying NOOOOO), but can we live without tyres? From the paddock to the plate, tyres are part and parcel of the product. Look around you right now and think about what didn’t arrive in your sight as a result of tyres’ involvement. I doubt if there is anything you see that didn’t arrive to you on tyres.

So why do we not engage with serious education not only for the personnel operating in the tyre industry but also the general public?

I read of tyre recycling efforts, yet most people will only identify with plastics as a recycling target. This whilst listening to a streaming service sitting on public transport running on transport that requires tyres to operate. Tyres are forgotten; everyone ASSuMEs[sic] that the tyre does its job without any thought given to the personnel that ensure our daily safety and food.

Tyres deserve better recognition of the service they provide to our societies. The personnel that service our tyres also deserve the highest level of training that can be provided, not just learn on the job with the potential of not being able to return home in the same condition as they arrived at work.

Training packages must be water tight; anything less will only result in the submersion of the outcomes below the standard that is safe. Training is an investment in the future; to those who invested in me in my younger days, I say THANK YOU! You did well in that I have made it to the later stages of my life intact and am still able to function. Your mentorship is remembered and honoured.

I take this opportunity to remember John Powath, the founder of this masthead. His standards and leadership have created opportunities for our industry to achieve a global recognition of excellence.

Training is the foundation of our industrial and societal processes. Do not scrimp on the materials presented and do not underestimate the risks involved regardless of how trivial they may seem.

Take care, stay safe and invest in your future by offering the highest quality training you can possibly deliver. Your life may depend upon it.”

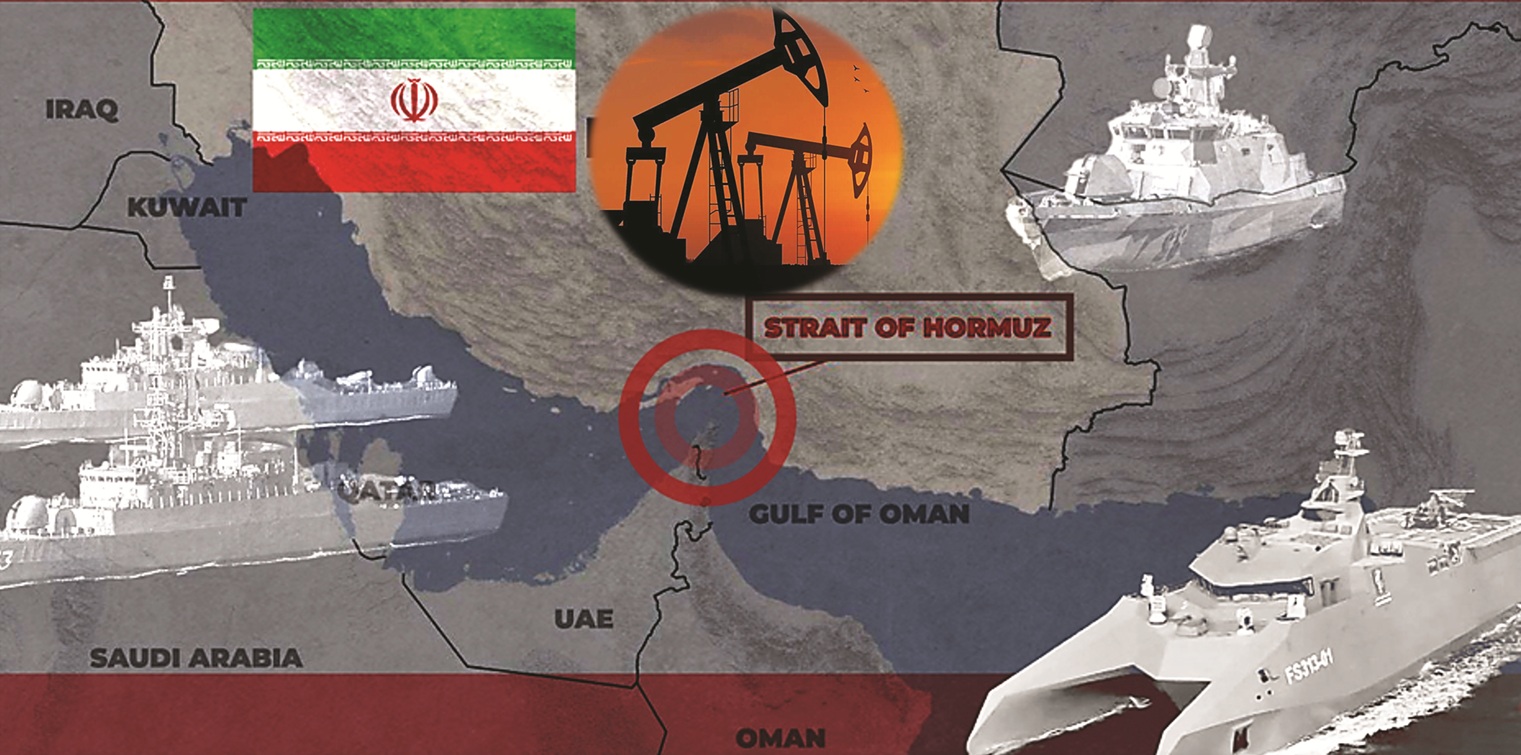

The Gulf Crisis Leading To A Profound Change In The Tyre Industry

- By Ertugrul Bahan

- June 15, 2026

The effects of the Strait of Hormuz closure will become particularly evident in 2026 and undoubtedly represent a strategic bottleneck for global energy and petrochemical trade. The Gulf War disrupted raw material supplies, crippled logistics and destabilised key export markets.

While the war represents a financial catastrophe, it also presents new opportunities. It has driven up raw material costs, while the logistics crisis has impacted export markets. The financial consequences include shrinking margins and reduced demand. However, long-term strategic shifts are expected, and these trends are likely to accelerate by 2040.

The closure of the Strait of Hormuz and the disruptions in the Red Sea have brought maritime traffic to the Middle East and Europe to a near standstill. The war has caused logistical chaos, and exports face immediate difficulties. China alone was expected to export more than seven million tyres to the Middle East by 2025, but this vital trade route is now blocked by skyrocketing freight rates and insurance premiums.

The profitability of the sector, whose gross margins are expected to fall to slightly more than four times their pre-war levels, is likely to be impacted by market consolidation and rising demand for high-tech tyres, particularly for electric vehicles. In the short to long term, the costs of raw materials such as synthetic rubber, carbon black and logistics are expected to rise significantly. Furthermore, this crisis could spur massive investments in bio-based and recycled materials to reduce dependence on petroleum. To address supply bottlenecks, the sharp decline in exports from the Middle East, coupled with significantly increased transportation costs, should be offset by regionalised production, for example, in India and Southeast Asia. With regard to product development, the short-term priority of cost control should lead to an acceleration of research and development into sustainable rubber compounds and sensorless smart tyres.

The end of the Gulf War is likely to usher in a period of weak economic growth and high inflation. The tyre industry is already facing a profound restructuring process. In the post-war era, the focus is not only on repairing the damage but, above all, on accelerating the long-term transition to regionalised supply chains, a circular economy and value creation through technology.

The most immediate consequence of war is a drastic increase in raw material costs,

which can account for almost 70 percent of tyre production costs. Around 45 percent of the raw materials used in the tyre industry are petroleum-based, and another 45 percent are natural rubber. In the case of synthetic rubber (NBR/SBR), the direct rise in oil prices leads to a price increase for butadiene, a key raw material. In the US, NBR prices rose by 7.4 percent at the beginning of March 2026; in China, butadiene prices jumped by 25 percent within a week.

Analysts estimate that this conflict could reduce global natural rubber production by 36 to 45 kilotonnes in the first half of 2026. How can this be explained, given that the effects on natural rubber are indirect? Diesel shortages prevent trucks from collecting rubber from plantations, thus reducing supply on the market. This shortage is contributing to the energy crisis in Southeast Asia. Prices for carbon black and chemicals derived from oil and gas are also rising in line with increasing energy costs. The supply of speciality chemicals (such as bromine from Israel) is also at risk.

Bio-based materials, particularly long-term ESG pilot projects, represent an immediate strategic necessity. The market for bio-based materials is projected to reach USD 337 million by 2032, with a compound annual growth rate (CAGR) of 101 percent, thus replacing volatile petrochemical feedstocks. Similarly, it is becoming increasingly clear that tyre pressure monitoring systems (TPMS) and sensorless, AI-powered systems like Michelin SmartWear can reduce costs and enhance safety.

Rising energy prices and crumbling infrastructure will weigh on consumption and investment. Inflation is high and is expected to remain high (around four percent for the G20 in 2026). Even after the war, energy costs and the rebuilding of supply chains will keep prices high. Consequently, the post-war economic recovery is expected to be slow and uneven, without a V-shaped rebound. The war has left lasting scars on global supply chains and public finances. Global GDP growth is weaker and below the pre-pandemic average.

In the field of carbon black recycling, carbon black is developing into a strategic raw material. Recycled carbon black (rCB) and tyre pyrolysis oil are becoming strategic raw materials intended to replace unstable fossil fuels. Massive investments, such as in Lummus-InnoVent, a continuous pyrolysis technology, will increase rCB production and reach a market of USD 15.6 billion by 2034.

Sustainable and bio-based materials are of great strategic importance, and significant investments are already being made to increase their production. Rising oil prices are making bio-based alternatives economically viable and essential for security of supply. Therefore, the transition to sustainable materials is no longer just an ESG goal but a necessity for the entire supply chain.

The Gulf War acted as a powerful catalyst, transforming promising future trends into immediate and essential investments. Bio-based silanes, for example, are now being used more and more frequently. Momentive’s NXT P97, a next-generation silane for electric vehicle tyres with 79 percent bio-based carbon, reduces reliance on fossil fuels while improving rolling resistance and durability. This technology, a prime example, is currently being deployed on a large scale.

The Gulf War acted as a powerful catalyst, transforming promising future trends into immediate and essential investments. Bio-based silanes, for example, are now being used more and more frequently. Momentive’s NXT P97, a next-generation silane for electric vehicle tyres with 79 percent bio-based carbon, reduces reliance on fossil fuels while improving rolling resistance and durability. This technology, a prime example, is currently being deployed on a large scale.

Tyre prices will remain high. The recovery will therefore be characterised more by rapid strategic development than by a simple return to pre-war levels. It is not so much the fluctuating demand from car manufacturers, but rather the replacement tyre market, which alone accounts for 70 percent of the volume, that is likely to continue to strongly support the consumer goods and logistics sectors during the economic recovery.

Increasing uncertainty is becoming the new normal. Geopolitical risks remain a key concern, forcing companies to prioritise resilience over efficiency. This situation is creating unequal competitive conditions for tyre manufacturers and their core markets. The difficulties faced by energy-importing countries in Europe and Asia will be further exacerbated in this climate of uncertainty.

This crisis will be one of the main reasons for the relocation of production to key markets, forcing the tyre industry to make unavoidable investments. It will be compelled to implement the technologies necessary for a more resilient, sustainable and technologically advanced future. New production centres will be established to circumvent geopolitical obstacles. This new dynamic is characterised by a clear strategic realignment of production and supply chains, accelerating ‘out-of-China’ models and leading to regionalisation. This conflict is not merely a disruption but a form of brutality for economically weaker countries, even if it represents a highly effective response to the relocation of production areas.

This war teaches us that excessive dependence on unstable regions like the Middle East must be balanced by the need for market diversification. Exporters like China and India will increasingly focus on Africa, Latin America and Southeast Asia. Margins will remain under pressure in the short term. High raw material and energy costs will not fall immediately. Large global companies will gain market share by leveraging their size and technology, as well as through increased regionalisation. Conversely, smaller, less diversified companies risk being acquired or exiting the market. Companies with strong pricing power and high operational efficiency will recover faster than those that rely solely on low prices.

The tyre industry is facing profound change. The tyre market is being restructured, and local, sales-oriented production is being intensified to circumvent geopolitical barriers and tariffs. In the short term, demand is expected to recover, but profit margins will be severely impacted by persistently high costs. In the long term, the sector will become more regionally focused, evolve towards a circular economy and rely more heavily on technology. In short, the end of the war will not restore the pre-conflict status quo. The crisis has forced a difficult but necessary transition to sustainable and resilient business models that will shape the key trends through 2040.

Fifty-seven years ago on 1st September 1968, I joined the rubber products manufacturing industry in Sri Lanka (then Ceylon) as a trainee in a medium scale footwear company. The only knowledge or rather awareness I had of rubber until that time was seeing the tapping of trees, adding a pungent liquid to the milky liquid, put on metal trays, squeezing the whitish slab of material through two rotating metal rollers manually rotated by a crank and putting them in a smoke shed that was available in some backyards to end up with a striped brownish sheet of rubber, which I later learnt was known as RSS. Later, in the early sixties, during our Organic Chemistry lessons, we learnt that C5H8 is the formula for Isoprene, which is the building block of natural rubber. Going down the memory lane of the past 57 years of knowledge acquisition in the rubber industry might turn out to be an exhaustive exercise. However, it is my sincere hope that some of my experiential insights might help the modern-day managers to seek areas that may strengthen their foundations in this era of rapid shifting sands.

I should say I am at a loss in finding an appropriate definition of knowledge from the vast interpretations which appear to be too academic. One practical and easy to understand definition I have come across in that knowledge is the ability to understand, apply and transfer information and experience to solve problems and adapt to changing circumstances, Merely the possession of facts is meaningless. It is the skill of using them effectively for survival, development and progress that is more important. It reminds me of the many research findings and innovations that are gathering dust in many institutions. In the case of early humans, knowledge emerged through direct observation of nature, trial and error and sharing same with groups. In my opinion, the context has virtually been the same over the ages, although the scope and the contents have undergone drastic changes during the course of human history, particularly through the four industrial revolutions and apparently heading for an unprecedented and a somewhat incomprehensible future.

If I am asked the question how I have acquired knowledge during my working life, I would say without any hesitation that it was through a process of osmosis. Those who studied botany under the biological sciences may perhaps vaguely remember how plants absorb water, minerals and other nutrients from the surrounding soil through their root systems by the process called osmosis. In a similar manner, we also acquire knowledge from the external environment through our sense facilities, namely the eyes, ears, nose, tongue and the skin, and through perceptions, which are processed by our brain and the central nervous system. The Buddhist doctrine gives a clear description of this process, which are well in line with the biological and physiological sciences. I, however, would not wish to go in to a philosophical deliberation at this point of time. Knowledge acquisition is a lifelong process with the ‘cradle to grave’ concept, and according to the modern scientific findings, starting at the moment of our conception in the mother’s womb.

I would now endeavour to delve a little into the knowledge acquisition modalities available to us trainees during our formative days of the career in the rubber industry from the late sixties onwards. The modern rubber technologist (if the term is still in use) may perhaps find them archaic as if they are viewing the archaeological remnants exhibited at a museum. It was hands-on experience from the beginning in what was termed a 3D industry, namely dirty, difficult and dangerous. This was mainly due to the particulate and dusty nature of the various fillers used such as carbon black and the toxicity of the rubber chemicals, coupled with the usage of high energy consuming motor driven machinery, both electrical and heat, usage of steam and compressed air, emission of high noise and vibration, fumes and high material load in some industries such as tyre manufacturing and tyre re-treading. The complexity and diversity are further aggravated by the macromolecular nature of both natural and synthetic rubber, which necessitates the somewhat illogical steps of breaking and remaking using a vast array of heterogeneous raw materials to facilitate the processability and for achieving the performance requirements of the products, some of which are of highly composite nature. As a consequence of the above, rubber product manufacturing industry was not at all the preferred choice for young school leavers like me. Hence, my entry into the rubber industry was due to the pure necessity of finding employment. However, the practical involvement with the identification and weighing of the multitude of rubber raw materials somehow had its attraction for me, which prompted me to read the limited number of text books and supplier literature that were available at that time. The real turning point in my career in the industry was the opportunity I got to follow the two-year part-time course at the then Ceylon College of Technology (now a university) to study for the Licentiate of the Institution of the Rubber Industry, LIRI (UK). This was equivalent to a full time BSc today. We were very fortunate to have three well-respected and dedicated teachers of the day in our quest for the acquisition of knowledge. Teaching was a noble profession for them, and I am very proud to state that their photographs adorn the entrance to the auditorium at the Plastics and Rubber Institute of Sri Lanka, where I joined as student in 1969 and ended up as its President for the year 2024.

Another remarkable feature during those days came in the shape of representatives from well-reputed giants in the raw material manufacturing companies such as Bayer, ICI, Monsanto, ACCI Rhien-Chemi and Polysar, names which to my knowledge are not existing now, or may be as mergers. These were invaluable opportunities for us the young technologists to gain the technical knowledge and discussion about the technical problems. The short technical sessions conducted by some of them in the evenings were eagerly awaited occasions during our days to share knowledge over a cup of tea. I am a little puzzled whether some of the similar events conducted online as webinars have the same effects or if at all that personal rapport.

The Bayers Technical Programme conducted annually at Thane, India, during those days was another avenue for gaining very valuable theoretical and practical knowledge, and I was fortunate to associate with prominent professionals such as R R Pandit, who left this world a few years ago, and Dr S N Chakravarthy.During my working with the Bata Shoe Company of Ceylon for 12 years, I had the opportunity to represent the company at a few of the Regional Technical Meetings held in the Far East. These were invaluable platforms for sharing knowledge and information of the technical developments of the individual companies. They were also enjoyable opportunities for networking and building up some lasting relationships. After following the programmes, it was compulsory that we give a presentation to the management and staff about our learning experiences, and more importantly, to plan development activities, the success of which was one criterion for our individual performance evaluation. Knowledge by itself is not power unless it is shared – a truism that will not apply to politics and the intelligence services. I well remember the case in a place I worked later about how some staff members who were sent to Japan for training deliberately skipped sharing what they learnt at company expense with the fellow staff members despite the several reminders.

As a passing remark, I may mention that my period of working in the tyre retreading and rubber products manufacturing companies in Kenya (for about 14 years) offered me the good opportunity of working with multiethnic communities while imparting my knowledge to train and develop staff members.

Now, coming to the global rubber product manufacturing, it can be seen that the focus on mixing, curing and reinforcement knowledge requirements has expanded into a multidisciplinary portfolio over the past 50 years, and the quest will continue. It is not prudent to do comparisons as ‘now and then’ because knowledge acquisition and its management is heavily dependent on the needs and requirements at any particular era or period of time. Unlike in our generation, a vast knowledge base, which is sometimes bewildering, is available at the touch of a fingertip for the modern-day managers, and apparently, most of it is related to their work and operational activities. My discussions and chats with many managers reveal the fact that they are overburdened with their daily activities and are working at different stress levels. They seldom seem to have any time or opportunity to integrate their work with the core values such as respect, gratuity and empathetical understanding.

The famous quote of Sir Issac Newton comes to my mind at this juncture: “If I have seen further, it is by standing on the shoulders of Giants.” He wrote this statement in a letter to Robert Hooke in February 1675, acknowledging that his own scientific discoveries were built upon the work of his predecessors, a sentiment that symbolises humility and scientific progress.

Knowledge and discipline go hand in hand. How to use knowledge appropriately needs discipline to comprehend. The consequences of using knowledge for the sake of knowledge, purely for application to industry, without giving due recognition to humanity and our core values is surfacing rapidly at the cost of trust, wellbeing, harmony and human development in every aspect of human activity, both locally and globally. In this respect, I remember the famous line from the poem, The Rime of the Ancient Mariner, by Samual Taylor Coleridge, which we happened to study in our literature class a long time ago.

‘Water, water everywhere and not a drop to drink’ illustrates the irony and anguish of being desperately hot and thirsty whilst being surrounded by nothing but ocean.

The author is a Management Counsellor from Sri Lanka.

Comments (0)

ADD COMMENT