Epsilon Carbon Launches N134 Specialised Hard Grade Carbon Black In India

- By TT News

- June 12, 2025

Epsilon Carbon, a leading global manufacturer of carbon black, has launched N134, which it claims is a specialised ‘Hard Grade’ carbon black known for its superior abrasion resistance and durability.

At present, the high-quality N134 grade is being imported due to the lack of consistent quality and supply chain issues in the Indian market. As a result, the tyre makers have to modify their formulations using other grades of carbon black, which it shared often leads to reduced performance.

But now, Epsilon Carbon has become the first company in India to install a dedicated manufacturing unit designed for N134 grade hard carbon. The company is expanding its existing Vijayanagar Carbon complex facility to produce 215,000 tonnes of carbon black.

This will not only ensure consistent supply of N134 carbon black for tyre makers in the country, reduce import dependency, but also open up export potential to markets such as Europe and USA. Epsilon Carbon will also focus on integrate advanced processing techniques to ensure batch consistency for durability and performance.

Vikram Handa, Managing Director, Epsilon Carbon, said, “This is a proud moment for us and for India’s carbon black manufacturing sector as the high quality N134 black will significantly reduce import dependency and provide tire manufacturers in India and abroad with a reliable, high-quality product. Our goal is to match global standards while building India’s capability to serve premium markets.”

- Association of Natural Rubber Producing Countries

- ANRPC

- Monthly NR Statistical Report

- Natural Rubber

ANRPC Publishes Monthly NR Statistical Report For June 2026

- By TT News

- July 31, 2026

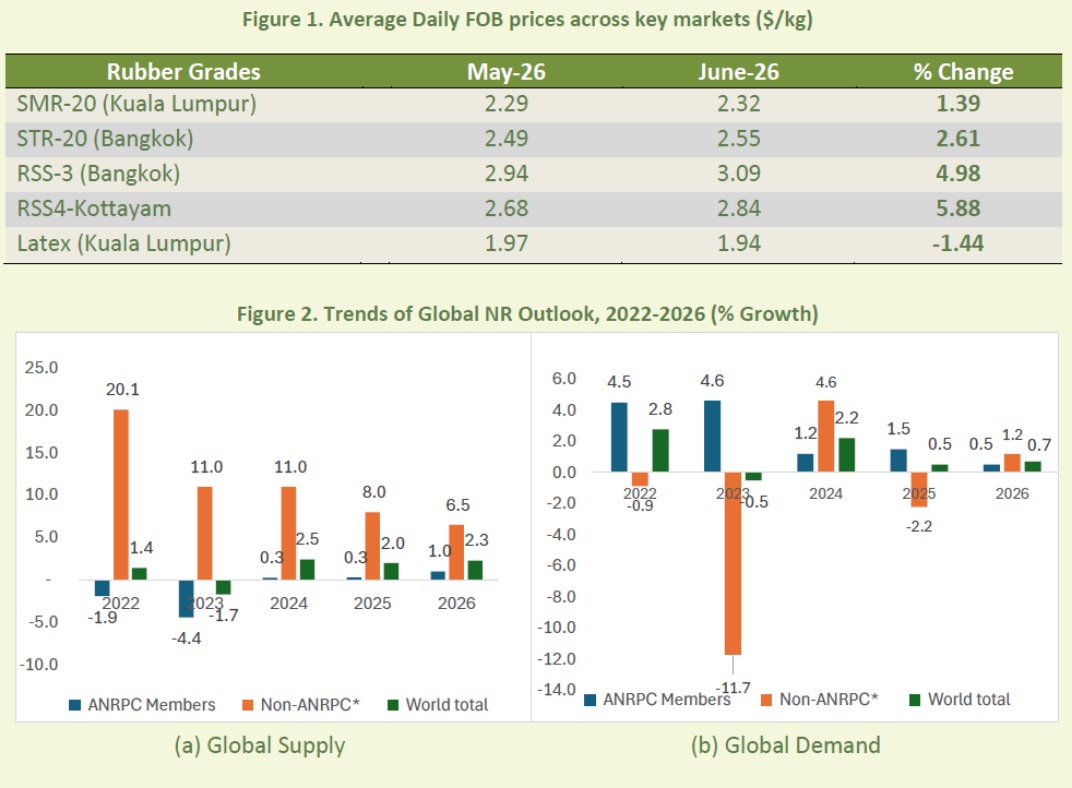

The Association of Natural Rubber Producing Countries (ANRPC) has released its Monthly Natural Rubber Statistical Report for June 2026, a month defined by price resilience amid conflicting market forces. The provisional reopening of the Strait of Hormuz triggered a sharp 20.29 percent drop in Brent crude oil prices to USD 85.40 per barrel. However, this bearish signal was counterbalanced by persistent supply constraints from El Niño-related weather disruptions across major producing regions.

Physical rubber prices posted broad-based gains across most grades. SMR-20 rose 1.39 percent to USD 2.32 per kilogramme, while STR-20 gained 2.61 percent to USD 2.55 per kilogramme. RSS-3 and RSS-4 advanced 4.98 percent and 5.88 percent to USD 3.09 and USD 2.84 per kilogramme, respectively, though latex eased 1.44 percent to USD 1.94 per kilogramme. On the trade front, China's imports surged 7.14 percent month-on-month, while India and Viet Nam declined. Export growth was recorded for Cambodia, Viet Nam and Indonesia, though Thai shipments contracted.

Global production for 2026 is projected at 15.310 million tonnes, up 2.3 percent from 2025, driven by gains in Thailand, China, India and Malaysia. However, June output fell 3.7 percent year-on-year to 1.207 million tonnes due to seasonal wintering and El Niño-related weather disruptions. Malaysia, Indonesia and Cambodia have introduced new incentive and governance measures to strengthen their sectors. Global consumption is forecast to grow 0.7 percent to 15.411 million tonnes in 2026, with June consumption rising 3.3 percent to 1.300 million tonnes, led by China and India amid steady tyre and EV-related demand.

Currency markets saw the Malaysian ringgit trade between RM3.96 and RM4.08 against the US dollar, while the Thai baht ranged from 32.56 to 33.24. In futures trading, the SHFE September 2026 contract averaged 17,580.68 CNY per tonne, down 0.45 percent month-on-month, while the SGX September contract averaged USD 2.24 per kilogramme, up 1.75 percent, with both reflecting tightening supply and firm downstream demand.

Pyrum Secures Long-Term Supply And Offtake Agreements With Pirelli

- By TT News

- July 31, 2026

Pyrum Innovations AG has finalised long-term supply and offtake agreements with Pirelli, reinforcing the tyre manufacturer’s European Tyre-to-Tyre initiative. The deal secures Pirelli’s purchase of Pyrum’s ThermoTireBlack (TTB) for use in its European production facilities, while Pirelli will provide Pyrum with end-of-life tyres from designated German sources.

These contracts simultaneously bolster Pyrum’s feedstock security and guarantee an industrial outlet for its recycled materials, covering both raw material procurement and product commercialisation. Through its proprietary thermolysis process, Pyrum transforms scrap tyres into ThermoTireBlack, which can substitute fossil-based carbon black, and ThermoTireOil (TTO), destined for chemical industry use. The partnership offers further validation of Pyrum’s technology within a certified European value chain involving tyre, chemical and synthetic-rubber leaders.

Pyrum also supports the broader Tyre-to-Tyre project, initiated by Pirelli with BASF and Synthos, which reintroduces secondary materials from used tyres and production waste into new tyre manufacturing via an ISCC PLUS-certified, traceable system.

Pascal Klein, CEO, Pyrum Innovations AG, said, “Signing these long-term agreements with Pirelli is an important commercial and strategic milestone for Pyrum. The coöperation secures both the supply of end-of-life tyres and an industrial outlet for our TTB. It confirms that our technology and products meet the requirements of one of the world’s leading tyre manufacturers and can contribute to the establishment of scalable circular value chains in Europe.”

MICHELIN ResiCare And IMCD Europe Forge Strategic Distribution Partnership For 5-HMF

- By TT News

- July 30, 2026

MICHELIN ResiCare, a specialist in renewable and high-performance chemical solutions, has entered into a distribution partnership with IMCD Europe, a major international distributor of speciality chemicals. The agreement centres on the European supply of 5-hydroxymethylfurfural (5-HMF), a bio-sourced compound produced at the company's Isère-based industrial facility in Péage-de-Roussillon.

Under the new arrangement, IMCD Europe will handle distribution across the continent while MICHELIN ResiCare maintains direct engagement with its key strategic accounts. The collaboration aims to significantly widen the molecule's availability to European manufacturers through an optimised logistics framework and localised technical support, thereby addressing rapidly growing demand within the materials and formulation chemical sectors.

The French production site, scheduled to begin operations in early 2027, will have an initial annual capacity of 3,000 metric tonnes. This domestic manufacturing capability represents a critical step in securing European access to a molecule deemed strategically important for the region's chemical industry, reducing reliance on external supply sources.

IMCD will contribute its technical expertise, market knowledge and pan-European distribution network to facilitate the integration of 5-HMF into new applications. The company's established footprint in polymers, advanced materials and speciality formulations positions it to provide developmental support to manufacturers exploring alternatives to fossil-derived intermediates. MICHELIN ResiCare has already spent two years assisting major industry players with application evaluations, and the partnership is expected to expand these efforts across a broader customer base.

Derived from fructose through non-toxic green chemistry and already REACH-registered, 5-HMF serves as a versatile building block for low-environmental-impact resins and can replace conventional petroleum-based ingredients across diverse industries including agriculture, cosmetics, construction, transport, aeronautics and electronics. The collaboration reinforces MICHELIN ResiCare's commitment to renewable resources and sustainable material development while aligning with IMCD's dedication to advancing innovation in greener chemistry solutions.

Laurent Lemonnier, CEO, MICHELIN ResiCare, said, “This partnership with IMCD represents a major step forward in our desire to popularise the use of 5-HMF and to support the transition to a more responsible chemistry. With its technical expertise, its capacity to support customers and its European location, IMCD is the perfect partner to speed up the distribution of this molecule of the future.”

Pirelli-Led Partnership Launches European Tyre-To-Tyre Recycling Initiative

- By TT News

- July 23, 2026

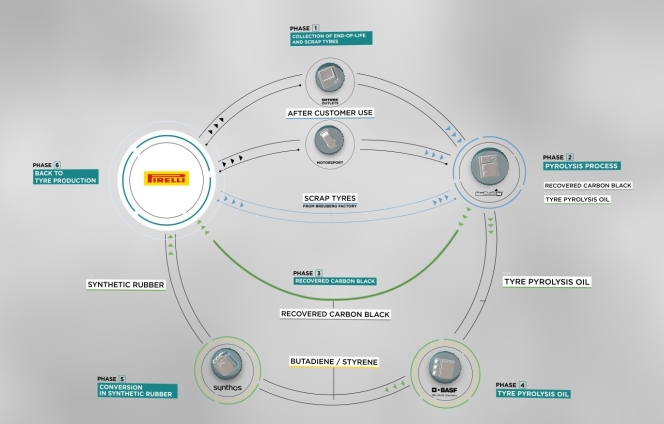

Pirelli, Pyrum, Synthos and BASF have launched a European tyre-to-tyre recycling initiative aimed at increasing the use of recycled materials from end-of-life and scrap tyres in the manufacture of new tyres. The project, coordinated by Pirelli, is designed to establish an industrial ecosystem that supports a circular economy while reducing reliance on virgin raw materials.

The initiative uses end-of-life tyres collected across Germany from selected Driver retail outlets and motorsport activities, together with scrap tyres from Pirelli's Breuberg manufacturing plant. These materials are processed into secondary raw materials, including synthetic rubber, certified under the ISCC PLUS scheme to ensure traceability throughout the value chain before being reintroduced into the production of new Pirelli tyres.

Under the process, Pyrum converts end-of-life and scrap tyres through pyrolysis into recovered carbon black (rCB) and tyre pyrolysis oil (TPO). The recovered carbon black is upgraded and used in Pirelli's European tyre production, replacing part of the virgin carbon black requirement.

The tyre pyrolysis oil is supplied to BASF, where it is co-fed with fossil-based feedstock in the production of chemicals including butadiene and styrene. Using a mass balance approach, the recycled content is allocated to ISCC PLUS-certified Ccycled® products. Synthos then uses these materials to manufacture ISCC PLUS-certified synthetic rubber for high-performance tyre applications, which is supplied back to Pirelli, completing the material loop.

The companies said the project demonstrates that large-scale product circularity requires collaboration across the value chain rather than action by a single company. The partnership combines material science, certified processes and industrial capabilities to recover, process and reuse materials within a structured system.

According to the companies, the project represents the most comprehensive application of a tyre-to-tyre circular model in Europe to date, showing how end-of-life tyres can be transformed into raw materials for new tyre production through a traceable industrial process.

Comments (0)

ADD COMMENT