Is Natural Rubber under mortal threat? Is there a possibility that factors like climate change, diseases etc. will bring the plantation industry to its knees?

It is a fact that the traditional rubber growing regions in almost all rubber producing countries in Asia are increasingly constrained by adverse effects of Climate Change. The yield from Hevea in traditional regions is impacted by extreme weather, recurrent cyclones, depression rains and flash floods. The last couple of years have seen interruption to tapping due to unforeseen rains and floods. Another major constraining factor is the recurrent outbreak of new diseases. For example, the outbreak of a new fungal leaf disease (Pestalotiopsis leaf fall disease) reported in Indonesia in 2018 has now spread into around 387,000 ha of mature rubber trees in the country. An estimated 141,000 ha in Thailand, 16,000 ha in Malaysia and 4,000 ha in Sri Lanka are reportedly affected by new fungal leaf diseases.

The low rubber prices that continued over several years resulted in poor maintenance of rubber holdings in almost all producing countries. As resource-starved farmers could not apply fertilizers or adopt proper crop protection measures over several years, rubber trees became weak and lost their resistance to diseases and extreme weather. It is striking to note that the root cause of the decline in yield is the unattractive prices and the resultant poor maintenance of holdings. A major trend reversal of prices can bring glaring positive changes in the natural rubber production sector. The potential national average yield (i.e., the annual production from a unit hectare of tapped trees) is 20 to 30% higher than what is realized now. For example, the average yield in India is currently 1,400 kg per hectare. But a favorable price can increase the average yield to the range of 1,750-1,800 kg. The country had realized the average yield of 1,823 kg in 2012 when the prices ruled high. Moreover, a large extent of mature trees which are currently left untapped in the country will come back to production once farmers find the prices attractive. The country has around 200,000 hectares of mature trees which are left untapped.

More specifically, it is the uneconomic return from the venture that hinders the natural rubber production sector. There is no mortal threat to the supply base as far as prices stay remunerative and the net profit from the venture is attractive. No industry can sustain for a long if it is economically unviable and natural rubber is no exception.

Can a COVID19 like pandemic impact NR industry long term? Do plantations have an effective healthcare plan to ensure labourers’ health and safety?

NR sector globally has almost fully recovered from the impact of the Covide-19. This is particularly true with reference to the global production, consumption, trade, and prices of natural rubber. The prices in key physical markets had crossed over the pre-covid level even by October 2020 and firmed up further since February 2021.

It is true that the production and processing sectors in Thailand and Malaysia are partly hindered as cross-border travel restrictions prevent migrant workers from neighboring countries to return to works. This issue, to a large extent, is resolved by making use of local workers by providing them necessary skills training. Coming to the downstream manufacturing sector, large number of debt-burden units in the MSME sector are reportedly struggling hard to bring their businesses back to normal. On the other side, large-scale manufacturing units, particularly those in auto-tyre manufacturing, have made V-shaped recovery driven by the pent-up momentum generated on lifting of the lockdowns. For healthcare rubber products such as rubber gloves, the epidemic has been a major boon. Taking the global rubber industry as a whole, the industry has already come out from the impact of the pandemic.

Workers engaged in large plantations are provided with social security and healthcare facilities as per the regulatory provisions being followed by the governments in the respective countries.

What are the chances of NR getting totally replaced by alternative rubbers? Will this happen? If so, how soon?

NR getting totally replaced by any alternative material is an impossible event in any case. The relative share of NR in the total quantity of new rubber (i.e., natural rubber and synthetic rubber) globally consumed was less than 30% during early 1970s. From that low level, the relative share of NR has gone up to nearly 50% as of now (47.2% in 2020). Synthetic rubber and natural rubber are not competing each other because technical considerations limit the scope of substitution between the two.

Lack of sufficient economic benefits is considered to be a reason for planters looking for alternate crops that can bring faster financial returns. How real is this? How much of rubber plantations have been replaced by other crops?

A total extent of nearly 0.6 million hectares of rubber trees was estimated to have cut down during 2015-2020 period in Thailand, Viet Nam, China, Malaysia, and India for cultivation of other crops or for conversion of land for non-farm uses. The details are given below:

|

|

Extent of rubber area discarded during the period 2015-2020 (Hectares) |

|

Thailand |

440,000 |

|

Viet Nam |

72,000 |

|

China |

46,000 |

|

Malaysia |

24,000 |

|

India |

4,000 |

In the case of Thailand, farmers are offered attractive cash incentive (More than US$3500 per hectare) by the government for removing aged rubber trees and planting other crops. It means, the shift from rubber in Thailand is largely policy driven. The case of Thailand is an exception. Generally speaking, the crop shift from rubber over the past few years is caused by the unattractive net profit from the venture.

Is plantation industry too slow to modernise itself, technologically as well as in terms of attracting skilled labor?

It is a fact that technological progress is severely constrained in the smallholder-dominated rubber production sector. The unattractive prices that prevailed over the period since 2015 made the farmers deprived of resources. Although high-yielding clones are available, farmers are generally postponing the replating of aged low-yielding trees due to their inability to meet the huge replanting cost. Another factor that prevents smallholders from replanting is the uncertainty of the farmers over the long-term prospects of rubber cultivation. Unattractive prices have also discouraged farmers from adopting good agricultural practices. Poor return from the venture has compelled farmers to discontinue the application of fertilizers, pest and disease management measures, and proper maintenance of holdings. Larger section of farmers has discontinued the use of stimulants and rain-guarded tapping. However, technological progress continued in large plantations owned by corporates, enterprises, and the public sector.

NR supply has always been unstable due to various reasons. Is this prompting manufacturers to look for other options?

There is no serios supply constraint or supply uncertainty as of now except the seasonal shortage. Moreover, all the producing countries have huge potential to increase their supply if the prices become attractive. This point was elaborated earlier.

Is there a campaign being run by alternative rubber sector to put pressure on NR industry?

As stated earlier, NR does not face any threat from alternatives basically due to the reason that the only substitute for natural rubber is natural rubber. In the total global consumption of new rubber (i.e., natural rubber plus synthetic rubber), the relative share of NR is currently around 50% (47.2% in 2020) as against less than 30% in early 1970s. There is no reason to anticipate a fall in the relative share of NR in the next three decades at least.

Are environmental sustainability factors detrimental to NR cultivation?

Environmental considerations can only help NR to gain preference over synthetic rubber, polyurethane, and other materials in various applications because natural rubber is recognised as “an environment-friendly industrial raw material and renewable resource”. The following points establish such a view:

- Rubber plantations purify atmosphere by absorbing CO2 and releasing O2. Based on scientific research undertaken by rubber research institutes in five countries, it is empirically proven that a hectare of rubber plantation annually sequesters as much as 30 tonnes of CO2 from atmosphere which is near to that of the Amazonian base.

- Rubber plantations are a good source of timber and bulk of this goes into furniture industry thereby protecting large extent of forests from being logged every year. Secondary branches of the rubber trees go into the fiber board industry and small twigs are used by the rural people as a source of firewood, both indirectly saving forests.

- Rubber plantations contribute to sustainable soil productivity. Soil productivity has not deteriorated in any of the traditional rubber growing countries which have the history of growing rubber for more than 100 years and already completed 3-4 rubber plantation cycles.

- One of the key factors which had adversely affected food crops production in the last couple of years was climate change. Rubber plantations offer solution to this as it helps balancing carbon level in atmosphere. Rubber is no longer a mono crop. Several food crops are grown along with rubber plants in all NR producing countries. The concept of raising rubber plantations as agro-forestry is being increasingly promoted across countries. It is common among rubber farmers to maintain a portion of their land for other crops. Moreover, rubber holdings provide sources of ancillary income through activities such as horticulture, fishery, honeybee, goat farming, etc.

- In all major natural rubber growing countries, rubber has been identified as a major tool of poverty alleviation and thus helping to achieve the Millennium Development Goals (MDGs).

Are there any concerted efforts being taken up by organisations like ANRPC, IRSG or governments that subsidise NR cultivation?

Developmental activities such as promotion of new-planting and replanting in each country are undertaken by the respective governments only. Among the member governments of ANRPC, Thailand, Malaysia, India, and Sri Lanka provide financial incentives to farmers to promote the cultivation of rubber. The governments usually mobilize the funds needed for the purpose from the same sector by levying a cess on the quantity of NR exported from the country or consumed within the country. The financial assistance cannot be termed as a ‘subsidy’ because the funds needed for the purposes are mobilized from the same sector.

Is it possible to have a globally uniform price structure for NR that can ensure interrupted supply?

In a market driven global economy, commodity prices are largely determined by the forces of supply and demand. This is particularly true in the case of NR which is a strategic industrial raw material coming from more than 10 million smallholder farmers world over. It is not practical to regulate NR prices globally as it is a real challenge to bring together all major producing countries and consuming countries for such a common agenda on terms acceptable to all. (TT)

INROAD And Rubber Board Launch Multilingual Training Videos For Rubber Growers

- By TT News

- August 06, 2026

The Rubber Board of India has launched a series of educational videos as part of the iSPEED (INROAD Skilling and Production Efficiency Enhancement Drive) programme, an INR 1.50-billion initiative aimed at enhancing skill development, quality improvement and infrastructure building within the natural rubber sector. This launch comes as the plantation activities under the larger Project INROAD (Indian Natural Rubber Operations for Assisted Development) in Northeast India approach completion, shifting focus towards productivity and quality enhancement through modern training and facilities.

The newly released video series targets nearly 300,000 rubber growers in the region, covering five essential processing areas: Rubber Tapping, Rain Guarding, Grading, Rubber Sheet Making and Scientific Smokehouses. To ensure broad accessibility, the modules have been produced in Assamese, Bengali, Hindi and Malayalam, enabling effective communication with diverse stakeholders across the natural rubber ecosystem.

The official release of the videos was conducted by Executive Director M Vasanthagesan, alongside Rubber Production Commissioner Dr Siju T Nair, other senior Board officials and representatives from the Indian tyre industry. Developed over the past year with technical assistance from the Rubber Board and the Rubber Research Institute of India, the educational content combines animation with real-life field demonstrations to simplify complex scientific practices for easy adoption.

Project INROAD represents a unique collaboration between the Indian tyre industry and the Rubber Board, with support from Apollo Tyres, CEAT, JK Tyre and MRF. Over the last five years, this partnership has facilitated new rubber plantations across approximately 180,000 hectares in 113 districts of Northeast India, establishing it as the country’s largest plantation development programme of its kind.

Mohan Kurian, Chairman, INROAD Project, said, "Skill development and adoption of scientific practices are essential for improving both productivity and quality in the natural rubber sector. These multilingual videos will serve as an effective training resource for growers and complement the Rubber Board's ongoing extension efforts across the country.”

Sanjiv Saxena, Convener, ATMA Supply Chain & Resources (SCR) Group, said, "The objective of the participating member companies under INROAD is to ensure that rubber growers benefit the most from a stronger natural rubber value chain. By improving productivity and quality, we aim to help farmers realise better returns while strengthening the sustainability of the entire ecosystem."

Muraligopal, who played a key role in coordinating the development of the videos, said, "These videos are the result of close collaboration with the Rubber Board, RRII and field teams across the Northeast. Their guidance and support helped us develop practical, farmer-friendly training modules based on scientific best practices."

Zeon And Yokohama Rubber Advance Sustainable Rubber Project With New Facility Completion

- By TT News

- August 04, 2026

Zeon Corporation has finalised the construction of a new bench-scale facility at its Tokuyama Plant in Shunan City, Yamaguchi Prefecture, dedicated to advancing the efficient production of butadiene from sustainable ethanol sources. The project, which broke ground in July 2025, represents a strategic move to establish a naphtha-independent raw material supply chain, thereby bolstering both corporate sustainability and the broader transition towards a carbon-neutral society. The facility is slated to commence full-scale operations in January 2027, with the ultimate goal of achieving commercial viability by 2034.

A commemorative ceremony took place at the plant site on 31 July 2026, drawing a total of 46 attendees. The gathering included official representatives from Japan’s Ministry of Economy, Trade and Industry (METI), the New Energy and Industrial Technology Development Organization (NEDO) and local governmental bodies from Yamaguchi Prefecture and Shunan City. Also present were delegates from the Yokohama Rubber Company, the construction contractor and various affiliated firms, alongside Zeon’s leadership, including Akira Honma, the Corporate Officer and Tokuyama Plant Manager.

This initiative forms one half of a dual-themed research and development programme undertaken in partnership with Yokohama Rubber, under the auspices of NEDO’s Green Innovation Fund. The collaborative effort is focused on the social implementation of technologies for synthesising both butadiene and isoprene from renewable biological materials by the 2030s. As part of this process, Zeon is set to produce a prototype polybutadiene rubber using the output from the new bench-scale facility, while Yokohama Rubber will subsequently manufacture test tyres from this material and conduct performance evaluations on test tracks.

Both companies have outlined a clear roadmap, intending to finalise the core technology for societal deployment by 2030 through the operation of a larger pilot plant, with full-scale commercialisation targeted for 2034. The bench-scale facility is a critical precursor in this phased approach, providing essential data for the scale-up process.

The broader project encompasses two selected NEDO themes, both subsidised through the Green Innovation Fund. The first involves the highly efficient synthesis of butadiene from ethanol, with technical cooperation from the National Institute of Advanced Industrial Science and Technology. The second focuses on biotechnological pathways to directly produce butadiene and isoprene from plant-based materials, involving partnerships with the Institute of Science Tokyo and RIKEN. Both tracks aim to supplement synthetic rubber feedstocks and support closed-loop recycling, aligning with Japan’s 2050 net-zero emissions goal by fostering long-term industrial innovation.

- Association of Natural Rubber Producing Countries

- ANRPC

- Monthly NR Statistical Report

- Natural Rubber

ANRPC Publishes Monthly NR Statistical Report For June 2026

- By TT News

- July 31, 2026

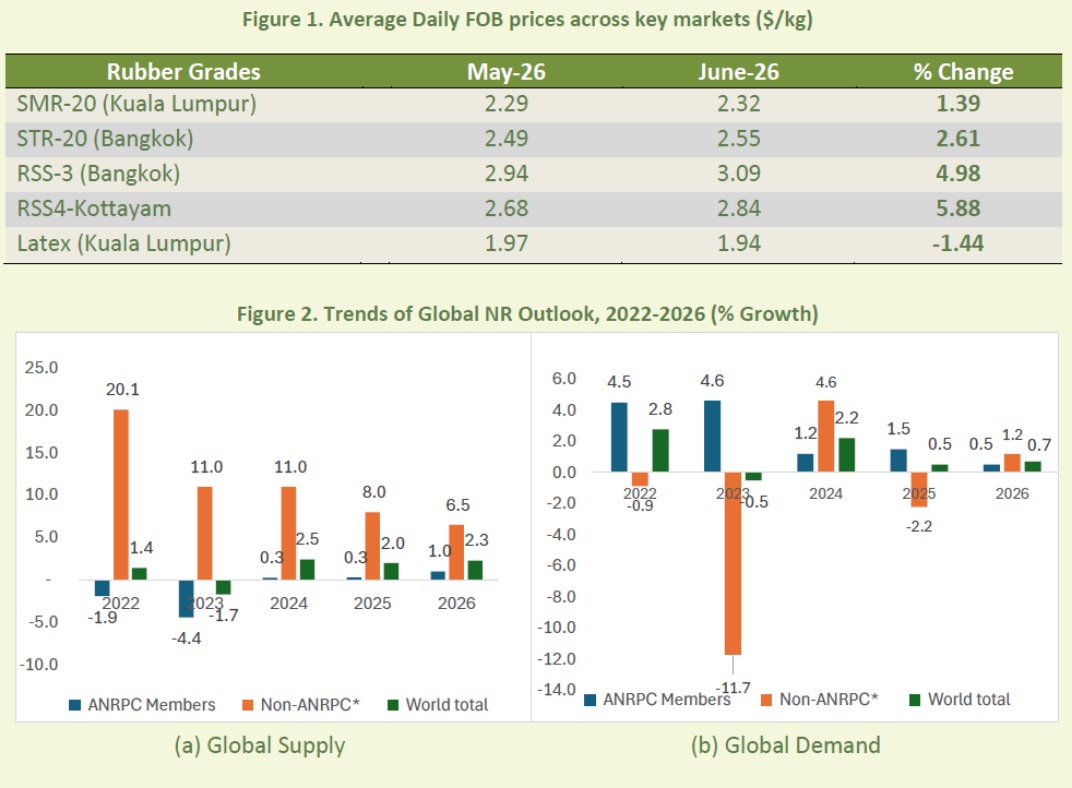

The Association of Natural Rubber Producing Countries (ANRPC) has released its Monthly Natural Rubber Statistical Report for June 2026, a month defined by price resilience amid conflicting market forces. The provisional reopening of the Strait of Hormuz triggered a sharp 20.29 percent drop in Brent crude oil prices to USD 85.40 per barrel. However, this bearish signal was counterbalanced by persistent supply constraints from El Niño-related weather disruptions across major producing regions.

Physical rubber prices posted broad-based gains across most grades. SMR-20 rose 1.39 percent to USD 2.32 per kilogramme, while STR-20 gained 2.61 percent to USD 2.55 per kilogramme. RSS-3 and RSS-4 advanced 4.98 percent and 5.88 percent to USD 3.09 and USD 2.84 per kilogramme, respectively, though latex eased 1.44 percent to USD 1.94 per kilogramme. On the trade front, China's imports surged 7.14 percent month-on-month, while India and Viet Nam declined. Export growth was recorded for Cambodia, Viet Nam and Indonesia, though Thai shipments contracted.

Global production for 2026 is projected at 15.310 million tonnes, up 2.3 percent from 2025, driven by gains in Thailand, China, India and Malaysia. However, June output fell 3.7 percent year-on-year to 1.207 million tonnes due to seasonal wintering and El Niño-related weather disruptions. Malaysia, Indonesia and Cambodia have introduced new incentive and governance measures to strengthen their sectors. Global consumption is forecast to grow 0.7 percent to 15.411 million tonnes in 2026, with June consumption rising 3.3 percent to 1.300 million tonnes, led by China and India amid steady tyre and EV-related demand.

Currency markets saw the Malaysian ringgit trade between RM3.96 and RM4.08 against the US dollar, while the Thai baht ranged from 32.56 to 33.24. In futures trading, the SHFE September 2026 contract averaged 17,580.68 CNY per tonne, down 0.45 percent month-on-month, while the SGX September contract averaged USD 2.24 per kilogramme, up 1.75 percent, with both reflecting tightening supply and firm downstream demand.

Pyrum Secures Long-Term Supply And Offtake Agreements With Pirelli

- By TT News

- July 31, 2026

Pyrum Innovations AG has finalised long-term supply and offtake agreements with Pirelli, reinforcing the tyre manufacturer’s European Tyre-to-Tyre initiative. The deal secures Pirelli’s purchase of Pyrum’s ThermoTireBlack (TTB) for use in its European production facilities, while Pirelli will provide Pyrum with end-of-life tyres from designated German sources.

These contracts simultaneously bolster Pyrum’s feedstock security and guarantee an industrial outlet for its recycled materials, covering both raw material procurement and product commercialisation. Through its proprietary thermolysis process, Pyrum transforms scrap tyres into ThermoTireBlack, which can substitute fossil-based carbon black, and ThermoTireOil (TTO), destined for chemical industry use. The partnership offers further validation of Pyrum’s technology within a certified European value chain involving tyre, chemical and synthetic-rubber leaders.

Pyrum also supports the broader Tyre-to-Tyre project, initiated by Pirelli with BASF and Synthos, which reintroduces secondary materials from used tyres and production waste into new tyre manufacturing via an ISCC PLUS-certified, traceable system.

Pascal Klein, CEO, Pyrum Innovations AG, said, “Signing these long-term agreements with Pirelli is an important commercial and strategic milestone for Pyrum. The coöperation secures both the supply of end-of-life tyres and an industrial outlet for our TTB. It confirms that our technology and products meet the requirements of one of the world’s leading tyre manufacturers and can contribute to the establishment of scalable circular value chains in Europe.”

Comments (0)

ADD COMMENT