Racing Tyres As A Branding Scheme

- By Gregers Lindvig

- August 20, 2021

The benefits of this are multiple. First of all, they don’t need to offer the full range of sizes to stake their claim as a racing tyre manufacturer. And I need to stress I’m talking about road car racing, not F1 racers, as those tyres are basically rocket science at this point. Many Chinese factories seem to have launched their racing tyre range for a very specific purpose, as they only have a few sizes, and sometimes very odd ones. For example, I saw a factory with just three different sizes for their racing tyre pattern, and one of them was 255/55R18. Just in case you want to rock your BMW X5 on the racing track, maybe? I can’t help but giggle at the image of drifting SUVs. Secondly, they don’t even need to be very good at it, or to be able to make very innovative products. It’s much easier to develop a product for a very specific purpose and just make it ‘good enough’, without engaging in the top five percent where all the heavy investment and R&D is needed to churn out those milliseconds that make all the difference for the top performers. Actually, when catering to the segment that just wants to burn tyres – drifters, for example – the usually all-important grip factor suddenly becomes negligible. And offering a budget option is attractive to those burning tyres on their own bill.

Design wise also racing tyres are very different from regular car tyres, in that they’re basically slicks with a flashy looking single lightning groove from close to the centre to the edge. Hard to make that design truly unique, but that also means that nobody can be blamed when designing something a bit too similar to something already on the market. Function before looks in this case, I’m sure. And in terms of rubber compounds, there are usually two or three different ones, depending on specific client needs, and they’re made to order. The hardest compounds are naturally for the drifters, and the softer ones for track racing.

But, in spite of the designs being simple, compounds not challenging to make, and the fact that the size range doesn’t need to be extensive, launching a racing tyre range still somehow reflects positively on all the regular passenger car tyres in the manufacturer’s range. As if the fact that they can design and produce tyres for high-performance racing machines also means that their standard range offers better handling or on-road performance to vehicles run by weekend warriors or others who might drive a station wagon, but really are race car drivers at heart.

That is, of course, if the Chinese budget manufacturers used this in their global marketing strategy – and in most cases, had one to begin with. The days where Chinese tyres could be sold on price alone are over, as output has far exceeded demand, but it’s striking to see how few have actually invested in their future market shares. For the layman, trying to name five major Chinese tyre manufacturers (or any of their brands) would be a tall order. Trying to name any that produce racing tyres would be even harder. Even for those inside the industry, very few know how many produce racing tyres or other specialised tyre products, because they often produce for a single client and don’t use this in active marketing. And no, a ‘sales manager’ posting a picture on LinkedIn doesn’t count. The brands and tyre manufacturers in China that will prevail are those able to build a global marketing strategy and naturally possess the skills to stay at the front of product development and gradually move out of the ultra-budget segment. The rest will learn the hardship of selling cheap tyres on price alone when China isn’t cheap anymore. (TT)

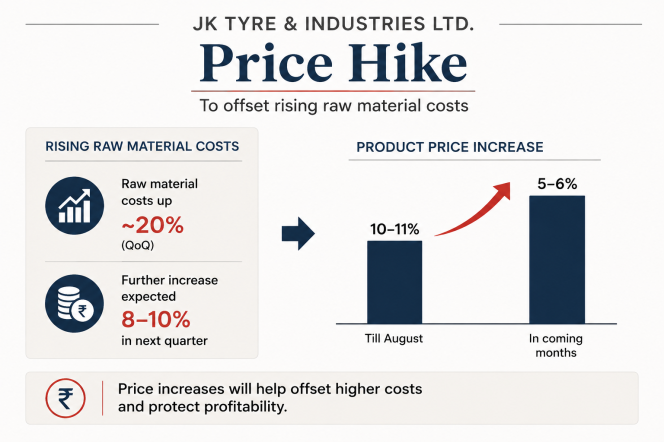

JK Tyre Raises Product Prices Amid Raw Material Surge

- By Sharad Matade

- August 11, 2026

JK Tyre & Industries has increased product prices and signalled further hikes as it seeks to offset rising raw material costs, even as demand remains resilient across segments.

The company said raw material prices rose about 20 percent quarter on quarter, with a further 8–10 percent increase expected in the following quarter. The increase has put pressure on margins, given that about 70 percent of tyre industry inputs are petro-based.

In response, JK Tyre raised product prices by 10–11 percent until August and plans an additional increase of 5–6 percent in the coming months to mitigate cost pressures.

The pricing action comes despite steady demand conditions. The company reported a 25 percent year-on-year increase in domestic volumes in the June quarter, supported by growth across both replacement and original equipment manufacturer segments.

Management indicated that demand remained stable across commercial vehicles, passenger vehicles and two- and three-wheelers, with no significant production cuts from OEM customers.

The company also said it continues to focus on premiumisation, with higher-margin products such as 16-inch and above passenger car tyres increasing their share in the sales mix.

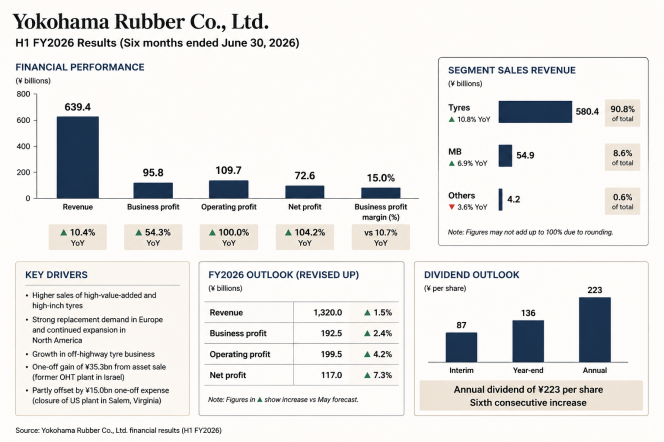

Yokohama Rubber H1 Profit Soars More than Double And Raises Full-Year Outlook

- By Sharad Matade

- August 11, 2026

Yokohama Rubber reported record earnings for the first half of fiscal 2026, with profits more than doubling and margins reaching a historic high.

The Japanese tyre maker said sales revenue rose 10.4 percent year on year to ¥639.4 billion in the six months to June, while business profit increased 54.3 percent to ¥95.8 billion. Operating profit doubled to ¥109.7 billion, and profit attributable to owners of the parent rose 104.2 percent to ¥72.6 billion.

Business profit margin improved to 15.0 percent, compared with 10.7 percent a year earlier, marking a record level for the company.

Yokohama Rubber said the results reflected strong performance across its businesses, delivering record first-half highs in all key earnings categories.

Segment data showed that tyre sales revenue rose 10.8 percent year on year to ¥580.4 billion, accounting for 90.8 percent of total revenue, while the MB (Multiple Businesses) segment recorded revenue of ¥54.9, up 6.9 percent and contributing 8.6 percent of the total. Other businesses declined 3.6 percent to ¥4.2 billion.

Business profit growth was led by the tyre segment, where profit increased 57.3 percent to ¥89 billion. The MB segment posted profit of ¥6.3 billion, up 22.5 percent, while other businesses reported profit of ¥0.5 billion.

The company said tyre segment growth was supported by higher sales of high-value-added and high-inch tyres, as well as increased volumes in the off-highway tyre business. Replacement tyre demand strengthened across regions, with strong sales in Europe and continued expansion in North America.

Operating profit was also supported by a ¥35.3 billion gain on the sale of assets at a former off-highway tyre plant in Israel, partly offset by a one-off expense of ¥15.0 billion related to the closure of a US tyre plant in Salem, Virginia.

The company also revised upwards its full-year forecast for fiscal 2026. It now expects sales revenue of ¥1,320 billion, business profit of ¥192.5 billion, operating profit of ¥199.5 billion and profit attributable to owners of the parent of ¥117 billion.

JK Tyre Reports Steady Quarterly Revenue As Margins Face Pressure

- By TT News

- August 10, 2026

JK Tyre & Industries reported broadly steady revenue for the first quarter of the financial year, with profitability constrained by higher input costs.

The company posted consolidated revenue of INR 39.56 billion for the quarter ended 30th June, 2026, while earnings before interest, tax, depreciation and amortisation (EBITDA) stood at INR 2.68 billion, implying a margin of 6.8 percent. Profit before tax was INR 0.54 billion and profit after tax came in at INR 0.43 billion.

According to the company’s financial statement, revenue from operations was INR 39.46 billion, compared with INR 38.69 billion in the corresponding period a year earlier.

Operating profit declined to INR 2.68 billion from INR 4.24 billionn a year earlier, reflecting pressure on margins.

Dr Raghupati Singhania, Chairman and Managing Director, said: “JK Tyre continued its steady performance in Q1FY27 with a consolidated turnover of INR 3.56 billion, supported by strong demand momentum across segments. The performance is driven by sharp focus on customer centricity, product excellence and disciplined execution across markets. During the quarter domestic volumes grew by 25 percent on year-on-year basis, across both replacement (12%) and OE markets (42%), with increasing contribution from higher-value added products. The continuing west Asis crisis led to a sharp increase in raw material prices which impacted our gross and operating margins. As is known approximately 70 percent of the tyre industry raw materials are petro based, hence, it is highly vulnerable to oil price movement”.

He added: “With a sharper focus on operating leverage, cost reductions, and increasing share of premium products, JK Tyre remains confident to improve performance in FY27 with double-digit revenue growth, aiming to create enduring value for all stakeholders with an increased profitability through strategic expansions”.

Dunlop And Beta Motorcycles Strengthen OE Ties With New Geomax Tyre Lineup

- By TT News

- August 08, 2026

Dunlop Motorcycle Europe has expanded its original equipment partnership with Beta Motorcycles, securing a deal to supply advanced Geomax tyres across the Italian brand’s trial and motocross lineups. The enhanced collaboration introduces new standard fitments for both competition disciplines.

For trial applications, the Geomax TL01 replaces the previous D803GP on Beta’s Evo and Sincro models. Engineered with a high-adhesion compound and a specialised block layout for angled terrain, the ultra-sticky tyre has already proven popular among Beta racers and now becomes factory-standard equipment.

In the motocross sector, Beta has adopted the Geomax MX34 for its entire RX range, covering both two-stroke and four-stroke 250 cc and 350 cc variants, as well as the 450 cc model. Designed primarily for intermediate ground, the versatile MX34 performs effectively across diverse surfaces, from soft mud to compacted dirt.

Donato Miglio, Race Team Manager Trial, Beta Motorcycles, said, "Geomax TL01 represents a significant step forward in performance, which is why we decided to adopt it as our original equipment trial tyre. Many of our riders already use it in competition, where it has proven its exceptional grip, stability and handling.”

Fabrizio Dini, Race Team Manager Motocross and Enduro, Beta Motorcycles, said, “In motocross, the latest generation of Dunlop MX tyres features significant performance improvements. Geomax MX34 provides excellent grip, particularly on dry surfaces, giving riders a reassuring feeling of safety and constant control. Both tyres suit our bikes perfectly.”

Miguel Morais, Original Equipment Manager, Dunlop Motorcycle Europe, said, “We are proud to deepen our partnership with Beta through the introduction of Geomax TL01 and MX34 across its latest trial and motocross models. Fitments like these are a strong endorsement of the capabilities of tyres throughout our range, and we’re excited that more and more riders will experience increased confidence and performance that helps them get the most out of their Beta motorcycles from their first ride.”

Comments (0)

ADD COMMENT