Smart mobility is as relevant as ever, with growing urbanisation rates in almost all countries across the globe. But the concept isn’t new. At least I recall reading about the future of driving when I was very young, and a university project concluded that in the future, cars would be able to connect to each other and slide onto some sort of rail system when driving on the highway, so nobody would have to worry about steering or speeding when covering the long stretches of the journey. Not surprising, the project couldn’t have been more wrong in its conclusion. But why didn’t it work? It would have reduced accidents, pollutant emissions, road wear and maintenance costs, and it would have probably been quite easy to develop guiding chips and software to let cars in and out of the chain.

Well, the answer is simple, and is proven by the fact that car sales are still going up worldwide in spite of an ever-growing range of alternative transportation methods available to the buyers: freedom. As global wealth keeps increasing, all societies can recognize that the first luxury people growing out of poverty take is to buy a car, in many cases even before considering taking out a mortgage to buy a house. Why do they do that? Obviously to signal their increased wealth to the people around them (it’s harder to show if your house is bought or rented), but also to enjoy the freedom of being able to go exactly where they want to go and when. In these corona times being able to move about without bumping into others in public transportation is of course also an important factor. If this wasn’t the case, car sales would be dropping rapidly. Public transportation is cheaper, if you compare it to total cost of ownership of a car it’s easy math, and in many cases it’s also faster and easier. Plus, you can be productive getting some work done or enjoying a good rest when you don’t have to sit at the wheel in a traffic jam.

For those who care about global warming and reducing the environmental impact, there’s even further incentive to get rid of the car, but still, this is not what we see in the new car sales figures – although you could argue that some people buy a new car because it pollutes less than the old one.

Bicycles

With all the new technology, it will be very interesting to see how smart mobility will be implemented in cities across the globe, and if it will change the trend for good. After all, it’s be big cities with massive population numbers that will make a difference for the planet. If we look at a city like Copenhagen, it has for many years focused on being the world’s best city to ride a bicycle in, and it has implemented many innovative structures allowing cyclists to zip from one place to another in a matter of minutes with minimal need to stop along the way. Some places bridges have been built just to cater to cyclists. No doubt you can get around faster and cheaper in Copenhagen if you ride a bike than by any other means of transportation.

Another thing that is becoming increasingly interesting in the big cities is the drone technology, now we have seen Chinese firefighters putting out high-rise fires using drones controlled from the ground, and many places they have also begun working as parcel or food delivery agents. But is there a viable case to argue that we will all be flying in private drone vessels instead of driving in cars in the coming decade? I wouldn’t bet my money on it. First of all, it would take long until the general public would trust a drone manufacturer enough to not fear dropping to the ground or being flung into a building or another drone mid-air at any moment. Second of all, they would most definitely run on electricity, which we know from electric cars means very heavy batteries and/or short operation times. Probably in colder regions you would also struggle with much lower performance during winter, and possibly weather conditions not allowing them to take off.

That’s another nightmare scenario – to be caught in a thunderstorm or hailstorm up in the air.

Naturally, the ultimate challenge would be that everyone would basically need to have a pilot license to operate them, and air traffic control would be an entirely new concept in this scenario. We have all seen movies like Stars Wars or The Fifth Element where flying vehicles somehow get into invisible lanes and layers, but it’s hard to see how that can go from fiction to reality.

Urban hubs

So, how can consumers most likely have their desire for freedom fulfilled within a smart mobility concept? Most likely by creating urban hubs or city line parking facilities, so it’s easy to take the car to, from, or between cities, but not inside them. At these hubs, you would park the car and jump on the next shuttle to anywhere in the city, or even ride a bike that you brought with you. Designing these hubs, along with ample green areas in the cities, is the only way that any city planner can create the grounds for real smart mobility, and not take people’s freedom away from them. Then the only thing left is to address the issue of the environmental impact caused by passenger cars, both combustion engine emissions and tyre pollution from wear during use and waste management at end of tyre life.

Tyre manufacturers don’t seem to be making huge changes to the technology yet, except for a few innovative products like the Michelin Tweel – and the ultimate challenge is of course that the vehicle so far has to be in contact with the road surface to move and handle satisfactorily. It’s hard to imagine any tyre concept where rubber against the road surface isn’t involved, and it’s also hard to imagine any tyre manufacturer supporting such a project, given the massive investments they have in their production equipment, which isn’t easy to readjust to put out something else. Well, at least not any serious manufacturer – there was a Chinese plant that stopped producing tyres this year to start producing face masks instead because of corona demand, but that probably says something about the quality of both products coming out of that factory, and it makes me very interested in reading their mission statement.

Ultimately, for tyre manufacturers to start investing in any game changing product development, we would have to see a development like we have seen with British Tobacco actually advertising against smoking – which is very much in line with the trends of the day but doesn’t seem rational from a business perspective. So, to conclude, I’ll venture a bet that we won’t see any drastic changes in how much smarter our mobility options will become until we either see a scenario that will allow people to experience the same level of freedom as owning a car, drastically reducing the environmental impact from driving and tyre waste, and/or creating cities where it utterly doesn’t make any sense to drive instead of hopping on the city’s smart mobility system, whatever that might turn out to be.

JK Tyre Raises Product Prices Amid Raw Material Surge

- By Sharad Matade

- August 11, 2026

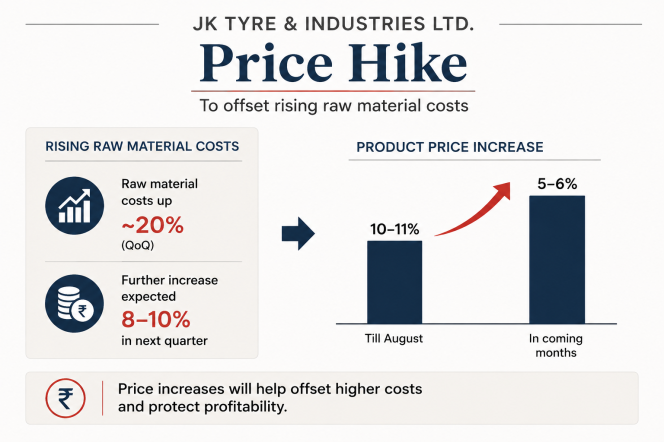

JK Tyre & Industries has increased product prices and signalled further hikes as it seeks to offset rising raw material costs, even as demand remains resilient across segments.

The company said raw material prices rose about 20 percent quarter on quarter, with a further 8–10 percent increase expected in the following quarter. The increase has put pressure on margins, given that about 70 percent of tyre industry inputs are petro-based.

In response, JK Tyre raised product prices by 10–11 percent until August and plans an additional increase of 5–6 percent in the coming months to mitigate cost pressures.

The pricing action comes despite steady demand conditions. The company reported a 25 percent year-on-year increase in domestic volumes in the June quarter, supported by growth across both replacement and original equipment manufacturer segments.

Management indicated that demand remained stable across commercial vehicles, passenger vehicles and two- and three-wheelers, with no significant production cuts from OEM customers.

The company also said it continues to focus on premiumisation, with higher-margin products such as 16-inch and above passenger car tyres increasing their share in the sales mix.

Yokohama Rubber H1 Profit Soars More than Double And Raises Full-Year Outlook

- By Sharad Matade

- August 11, 2026

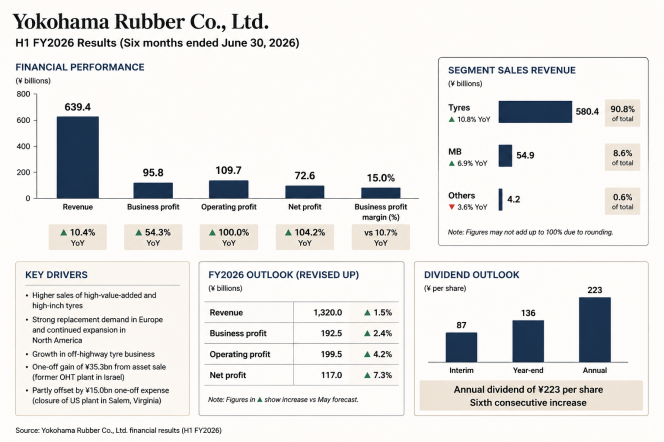

Yokohama Rubber reported record earnings for the first half of fiscal 2026, with profits more than doubling and margins reaching a historic high.

The Japanese tyre maker said sales revenue rose 10.4 percent year on year to ¥639.4 billion in the six months to June, while business profit increased 54.3 percent to ¥95.8 billion. Operating profit doubled to ¥109.7 billion, and profit attributable to owners of the parent rose 104.2 percent to ¥72.6 billion.

Business profit margin improved to 15.0 percent, compared with 10.7 percent a year earlier, marking a record level for the company.

Yokohama Rubber said the results reflected strong performance across its businesses, delivering record first-half highs in all key earnings categories.

Segment data showed that tyre sales revenue rose 10.8 percent year on year to ¥580.4 billion, accounting for 90.8 percent of total revenue, while the MB (Multiple Businesses) segment recorded revenue of ¥54.9, up 6.9 percent and contributing 8.6 percent of the total. Other businesses declined 3.6 percent to ¥4.2 billion.

Business profit growth was led by the tyre segment, where profit increased 57.3 percent to ¥89 billion. The MB segment posted profit of ¥6.3 billion, up 22.5 percent, while other businesses reported profit of ¥0.5 billion.

The company said tyre segment growth was supported by higher sales of high-value-added and high-inch tyres, as well as increased volumes in the off-highway tyre business. Replacement tyre demand strengthened across regions, with strong sales in Europe and continued expansion in North America.

Operating profit was also supported by a ¥35.3 billion gain on the sale of assets at a former off-highway tyre plant in Israel, partly offset by a one-off expense of ¥15.0 billion related to the closure of a US tyre plant in Salem, Virginia.

The company also revised upwards its full-year forecast for fiscal 2026. It now expects sales revenue of ¥1,320 billion, business profit of ¥192.5 billion, operating profit of ¥199.5 billion and profit attributable to owners of the parent of ¥117 billion.

JK Tyre Reports Steady Quarterly Revenue As Margins Face Pressure

- By TT News

- August 10, 2026

JK Tyre & Industries reported broadly steady revenue for the first quarter of the financial year, with profitability constrained by higher input costs.

The company posted consolidated revenue of INR 39.56 billion for the quarter ended 30th June, 2026, while earnings before interest, tax, depreciation and amortisation (EBITDA) stood at INR 2.68 billion, implying a margin of 6.8 percent. Profit before tax was INR 0.54 billion and profit after tax came in at INR 0.43 billion.

According to the company’s financial statement, revenue from operations was INR 39.46 billion, compared with INR 38.69 billion in the corresponding period a year earlier.

Operating profit declined to INR 2.68 billion from INR 4.24 billionn a year earlier, reflecting pressure on margins.

Dr Raghupati Singhania, Chairman and Managing Director, said: “JK Tyre continued its steady performance in Q1FY27 with a consolidated turnover of INR 3.56 billion, supported by strong demand momentum across segments. The performance is driven by sharp focus on customer centricity, product excellence and disciplined execution across markets. During the quarter domestic volumes grew by 25 percent on year-on-year basis, across both replacement (12%) and OE markets (42%), with increasing contribution from higher-value added products. The continuing west Asis crisis led to a sharp increase in raw material prices which impacted our gross and operating margins. As is known approximately 70 percent of the tyre industry raw materials are petro based, hence, it is highly vulnerable to oil price movement”.

He added: “With a sharper focus on operating leverage, cost reductions, and increasing share of premium products, JK Tyre remains confident to improve performance in FY27 with double-digit revenue growth, aiming to create enduring value for all stakeholders with an increased profitability through strategic expansions”.

Dunlop And Beta Motorcycles Strengthen OE Ties With New Geomax Tyre Lineup

- By TT News

- August 08, 2026

Dunlop Motorcycle Europe has expanded its original equipment partnership with Beta Motorcycles, securing a deal to supply advanced Geomax tyres across the Italian brand’s trial and motocross lineups. The enhanced collaboration introduces new standard fitments for both competition disciplines.

For trial applications, the Geomax TL01 replaces the previous D803GP on Beta’s Evo and Sincro models. Engineered with a high-adhesion compound and a specialised block layout for angled terrain, the ultra-sticky tyre has already proven popular among Beta racers and now becomes factory-standard equipment.

In the motocross sector, Beta has adopted the Geomax MX34 for its entire RX range, covering both two-stroke and four-stroke 250 cc and 350 cc variants, as well as the 450 cc model. Designed primarily for intermediate ground, the versatile MX34 performs effectively across diverse surfaces, from soft mud to compacted dirt.

Donato Miglio, Race Team Manager Trial, Beta Motorcycles, said, "Geomax TL01 represents a significant step forward in performance, which is why we decided to adopt it as our original equipment trial tyre. Many of our riders already use it in competition, where it has proven its exceptional grip, stability and handling.”

Fabrizio Dini, Race Team Manager Motocross and Enduro, Beta Motorcycles, said, “In motocross, the latest generation of Dunlop MX tyres features significant performance improvements. Geomax MX34 provides excellent grip, particularly on dry surfaces, giving riders a reassuring feeling of safety and constant control. Both tyres suit our bikes perfectly.”

Miguel Morais, Original Equipment Manager, Dunlop Motorcycle Europe, said, “We are proud to deepen our partnership with Beta through the introduction of Geomax TL01 and MX34 across its latest trial and motocross models. Fitments like these are a strong endorsement of the capabilities of tyres throughout our range, and we’re excited that more and more riders will experience increased confidence and performance that helps them get the most out of their Beta motorcycles from their first ride.”

Comments (0)

ADD COMMENT